📈 The state of American entrepreneurship: everything you should know

My conversation with John Dearie of the Center for American Entrepreneurship

A dynamic economy is one that constantly reallocates capital and workers to where they can be used most productively. A key mechanism for this process of economic growth is the creation of new businesses. And that process has been on the decline for decades, although there’s been an upturn since the pandemic began.

To find out more about what’s happening with American entrepreneurship, I contacted my friend John Dearie, founder of the Center for American Entrepreneurship.

➡ On the long-term state of American entrepreneurship …

When I first heard back in 2011 that entrepreneurship in the United States was in decline, I didn’t believe it. After all, the United States is regarded as the world’s most entrepreneurial nation, the home of Intel, Microsoft, Apple, Google, Amazon, Facebook, and many other examples of the most innovative and consequential companies on earth, home to Silicon Valley and Shark Tank — how could American entrepreneurship be in decline?

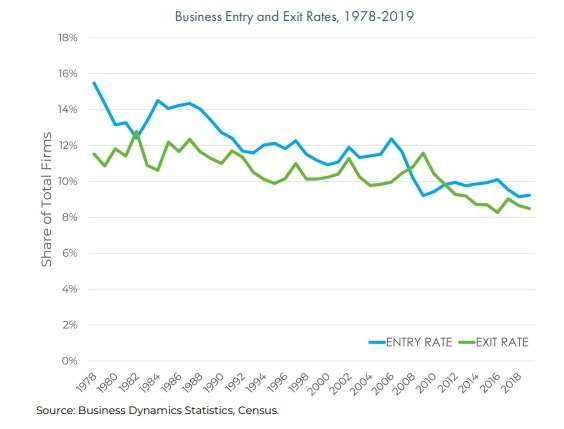

But after looking carefully at the work of people like Bob Litan and Ian Hathaway at the Brookings Institution, Nobel Prize laureate Ed Prescott, Lee Ohanian at Stanford, the Kauffman Foundation, and data collected by the Census Bureau, the decline in new business formation was undeniable. After remaining remarkably consistent for decades, the number of new businesses launched in the United States peaked in 2006 and then began a precipitous decline — a decline accelerated by the Great Recession.

From 2002 to 2006, the US economy produced an average of about 525,000 new employer firms each year. Between 2009 and 2019, however, the number of new businesses launched annually dropped to about 400,000, meaning that over that 10-year period the United States experienced a startup deficit of 100,000 new firms every year — a million missing startups over that period compared to historical trends.

Even more alarming, Bob and Ian had shown that rates of entrepreneurship — the fraction of all US businesses that are new — had fallen by half since 1978, and that the decline had occurred in all 50 states, in all but a handful of the 360 metro areas they examined, and across a broad range of industry sectors.

This was all quite alarming because repeated research had also demonstrated that startups account disproportionately for the innovations that drive productivity growth, economic growth, and net new job creation.

➡ On what’s he’s learned about the causes of the dynamism downshift …

I was the policy director at the Financial Services Forum at the time, and I and my colleague, Courtney Geduldig, thought about it for a few weeks and finally came to a pretty simple but apparently radical conclusion — if you want to know what’s going on with American entrepreneurs, get the hell out of Washington and go ask them.

So that’s what we did. With the Forum’s permission and support, Courtney and I hit the road in the summer of 2011 and conducted roundtables with entrepreneurs all across the country. We asked them a very simply question: “What’s in your way?”

What we heard in response astonished us. Despite a few differences in what you might call regional emphasis, we heard the same half a dozen issues or complaints everywhere we went:

“The country isn’t investing enough in innovation.”

“There’s not enough people with the skills that we need.”

“Our immigration policies are insane.”

“Not all good ideas are getting funded.”

“Regulatory complexity and uncertainty are killing us.”

“Tax complexity is a major distraction and aspects of the tax code are hostile to startups and their investors.”

“There’s too much economic uncertainty — and it’s Washington’s fault.”

It was the most fascinating experience in my professional life and changed the trajectory of my career, which up until that point had been a career in banking and financial policy, first at the Federal Reserve Bank of New York for nine years, followed by 17 years at the Forum.

It occurred to me that what we had learned on the road with America’s entrepreneurs was incredibly significant. So, I decided to write a book about our experience — a book that would report on what entrepreneurs across the country had told us and take a first crack at a policy agenda intended to address the problems and challenges entrepreneurs had pointed to. That book was Where the Jobs Are: Entrepreneurship and the Soul of the American Economy, which was published by Wiley in early 2014.

➡ On the surge of entrepreneurial activity during the pandemic …

I’m still not sure what the spike in new business applications will mean in the longer run. Some have interpreted the spike as the long-awaited recovery in entrepreneurship. It may be, but my instincts tell me that we haven’t seen enough to declare that the kind of entrepreneurship that America needs — disruptive, innovation-driven, productivity- and growth-driving entrepreneurship — has really turned the corner.

As the pandemic set in during the initial months of 2020, entrepreneurship plunged as measured by new business applications tracked by the Census Bureau. That’s exactly what happened during the 2008 financial crisis and Great Recession, so the initial plunge was not a surprise. But starting in April of that year, new business applications began to surge and the surge continued for the remainder of the year. For the full year, new applications reached nearly 4.5 million in 2020, a 24 percent jump from 2019, and 50 percent higher than the annual average over the previous decade. The surge continued through 2021 and 2022, although at somewhat slower pace.

In my view, the difference between 2008 and 2020 in terms of new business applications can be explained by the difference in the nature of the two recessions. The Great Recession was caused by a historic financial crisis that nearly wrecked the banking system and caused home prices and financial markets to crash. So, when millions of people lost their jobs, they had the occasion to become entrepreneurs, but not the capital they needed. Their savings and financial assets had dwindled, home equity had disappeared for many, angel and venture capital got much more selective, and banks slashed lending and revolving credit.

By stark contrast, the 2020 recession was manufactured when the economy was deliberately shut down to combat the virus. There was no financial crisis, and sources of startup capital available to people who lost their jobs — savings, financial assets, and home equity — were strong and reinforced by generous government support programs. The stock market plunged initially, but then recovered fairly quickly. So, in 2020, you had both the occasion for new business formation — “entrepreneurship of necessity” — and the capital required for people to act. In fact, there’s evidence that many people used their unemployment checks to start new businesses.

On the other hand, the Census Bureau has shown that a large portion of the spike in new business applications has been in the “non-store retail” category — people selling products online — so many of these new businesses are sole-proprietorships unlikely to grow quickly or create many jobs. Given that reality, I’ve been somewhat skeptical about the longer-term significance of the spike. But more recent Census Bureau data has shown that not only has the surge in new applications continued through 2021 and 2022, the number of applications by new businesses likely to be employers — so-called “high propensity firms” — reached an all-time high in 2021. So, something very interesting — and potentially exciting — is clearly underway. We’ll have to keep watching.

➡ On whether the pandemic will have any effect on long-run trends in entrepreneurship/business formation rates …

I think there are three profound pro-entrepreneurship changes in the US economy, and American society generally, stemming directly from the pandemic that will persist long-term — and I expect at least two will be permanent.

The first is the change in mindset regarding work as a result of the pandemic — whether to work, the importance of work in people’s broader lives, the kind of work people are willing to do, and under what circumstances. Covid has reminded us all how fragile and finite life is. And I think that stark reminder has caused a society-wide reevaluation of what’s important, where we’re all at in our lives, and what we want to enjoy, try, and accomplish in the limited time we have left. That reevaluation is what’s driving the “Great Resignation” and it is at least part of what’s driving the spike in entrepreneurship. Millions of Americans are saying “screw this job that I hate — I’m ready to try that idea I’ve had in the back of my head for years.” I’m not sure if that fundamental reevaluation and resetting of values will be permanent, but I think it will last for some time.

The second pandemic-related change is remote work. By way of the pandemic lock-down, people learned that they can be just as productive, contribute just as much to teams, and deliver the same value from home — and they don’t have to suffer through the time-sink and expense of a commute. They learned how to use the tools of remote work, they’ve grown accustomed to the experience and its advantages, and they like it. Yes, many businesses are trying to get employees back into the office and some will succeed to some extent. But my guess is that the American workplace will never be the same. At best, most employers will be able to require employees to be on-site a couple of days a week or every other week.

And that’s game-changing for entrepreneurs. It becomes much easier to secure the talent they need because their employees can be anywhere. For example, it has helped American entrepreneurs innovate around our idiotic immigration policies — they no longer have to get foreign-born talent into the country. I know many startups whose entire workforce is spread either around the country or around the globe.

The third profound pandemic-driven trend that I expect will be permanent — and it’s related to, and reinforcing of, remote work — is the digitalization of new and small businesses. Forced by local restrictions to limit foot traffic in stores, or to close physical locations entirely, new and small businesses increasingly turned to online platforms like Facebook, eBay, Amazon, Google, and Shopify to open digital storefronts, social media sites like Instagram and Twitter to market to customers, video conferencing platforms like Zoom and Microsoft Teams to interact with suppliers and pitch potential investors, and digital payment tools like PayPal, Venmo, and Square.

➡ On why he’s confident that the impact of digitalization is here to stay …

The digitalization of new and small business is here to stay and it is powerfully pro-entrepreneurship. Technology has dramatically reduced the costs of starting a business, finding and cultivating customers, marketing, selling, getting paid, and finding investors.

According to a State of Small Business Report published in December of 2021 by the Small Business Roundtable and Facebook, 51 percent of small businesses reported increasing their online interactions with customers, 35 percent had expanded the use of digital payments, and more than a third of businesses that use online tools reported conducting all of their sales online. In 2021, PayPal reported triple the typical quarterly growth in new merchant accounts.

The trend toward the digitalization of business has been underway for years, but Covid dramatically accelerated the shift — in large part because of the warm embrace by the American consumer. According to an analysis by consulting firm McKinsey & Co., the pandemic compressed into months the adoption of e-commerce by customers that would have otherwise taken 10 years, with three out of four Americans having tried a new shopping method due to the coronavirus.

Particularly significant is that the acceleration to online shopping extends to older consumers. A survey released in late 2021 by digital consulting firm Mobiquity found a 47 percent increase in the number of baby boomers reporting that they had ordered delivery from a restaurant through a website or app; a 193 percent increase in the number ordering groceries online; and a 469 percent increase in the number who have used tele-medicine.

➡ On whether the forces that led to the downward trend in entrepreneurship in recent decades have abated, or whether the recent surge been caused by new pro-dynamism forces …

Whether the increase in new business formation persists and even strengthens or is short-lived depends a lot on what policymakers do to support entrepreneurship. That’s especially true because there’s a good chance of at least a mild recession in 2023. Entrepreneurship is very risky and startups — though hugely important — are exceptionally fragile. They’re like toddlers — lots of potential, but easily knocked off their feet. Even under the best of circumstances, a third of all new businesses fail by their second year, half by their fifth. If economic conditions deteriorate in the first half of 2023, as many expect they will, it can be expected that a good portion of the new business launched since the onset of the pandemic will fail.

With that in mind, the spike in new business applications should not be interpreted by policymakers as an excuse to conclude that American entrepreneurship is thriving and, therefore, unworthy of their attention and action. Rather, the rise in the number of Americans taking the considerable risk to strike out on their own to create and build something new should be seen as an urgent opportunity — a call to decisive action. Policymakers should pursue a bold pro-entrepreneurship and -innovation agenda that reinforces the recent surge — that supports those that have taken the leap and that encourages others to do the same. The stark reality is that most of the barriers, obstacles, and risks that have undermined entrepreneurship in recent decades remain. We still have lots of work to do, and 2023 is a great year to do it.

➡ On what lawmakers in Washington should be doing to boost business formation and entrepreneurship …

There’s still lots of work to do regarding the obstacles and challenges revealed by those original roundtables in 2011 that I wrote about in my book — investing more federal resources in innovation; improving access to skilled talent, which includes education and immigration reform; better access to capital; regulatory relief; and a tax code that is supportive of entrepreneurs and their investors. Those are the fundamental issues that still comprise CAE’s agenda. (Folks can read more about those issues, and our proposed solutions, at www.startupsUSA.org.)

I should mention quickly that passage of the CHIPS and Science Act this past August is a major step in the right direction toward reversing the 60-year decline in government investment in research and science. The act invests $280 billion to bolster R&D, secure America’s access to the advanced semiconductors that power everything from smartphones to fighter jets, and create 20 regional innovation hubs, which will be a huge catalyst of regional economic development.

There’s just one problem — we don’t have the workforce needed to implement the act. To fulfill the extraordinary promise of the CHIPS and Science Act and secure America’s innovation future, policymakers must act now to pass commensurately bold workforce development policies — including high-skilled immigration reform, as I argued in this Op/Ed published just last week.

To those basic agenda issues mentioned above, we’ve added a number of other issues that have to do with de-risking entrepreneurship — making it easier for people to leave the corporate job to pursue an entrepreneurial venture. When Joe Biden landed in Rome for the G20 summit on October 29, 2021, he represented the only G20 member with no paid family leave or national childcare policy, and one of only two members — the other being Indonesia — without universal access to healthcare.

The charge that policies like universal healthcare, paid family leave, and national childcare are “socialism,” or at least socialistic, stands in stark contrast to the importance of such policies to something quintessentially American and capitalistic — entrepreneurship.

Since launching CAE, my colleagues and I have continued to conduct roundtables with entrepreneurs across the country on a regular basis to stay in close touch with them, their needs, challenges, and priorities — to make sure we’re focused on the right issues in the right way. In five years, we’ve conducted about 40 roundtables, or about eight each year.

➡ On what those rountables have taught him …

At our roundtables — in addition to the basic issues mentioned above — four topics invariably come up: healthcare, childcare, student debt, and retirement security. Each represents a major risk for would-be entrepreneurs inclined to launch a new business and a major obstacle to attracting and retaining the skilled talent that new businesses need to survive and grow.

To learn more about these “life risks” and their impact on American entrepreneurship, we conducted a roundtable focused specifically on those issues on October 29, 2021 with 10 entrepreneurs from six states. I reported on the roundtable in a piece I wrote called “Social Infrastructure Isn’t Socialism — It’s Pro-Entrepreneurship.” Their candid comments, shared experiences, and remarkable insights reveal just how critical these issues are to America’s entrepreneurs and innovators — particularly women founders — and how high the stakes really are as policymakers continue to debate potential solutions.

On the good news front, the “SECURE 2.0” Act was enacted as part of the Omnibus spending bill passed by Congress and signed by the president on December 23rd. The act makes a number of important changes to retirement security law that will dramatically enhance retirement savings for entrepreneurs, their employees, and gig economy workers. Now we need similar progress on the other critical fronts.

These are complex issues deserving of vigorous debate. But, at the end of the day, I’d argue that we as a nation and as a society need to decide whether we simply like thinking about ourselves as the world’s greatest entrepreneurship nation, or whether we want to really be the world’s greatest entrepreneurship nation.

America’s entrepreneurs have told us what they need to thrive. I think we should believe them.

This is so informative.

“At our roundtables — in addition to the basic issues mentioned above — four topics invariably come up: healthcare, childcare, student debt, and retirement security. Each represents a major risk for would-be entrepreneurs inclined to launch a new business and a major obstacle to attracting and retaining the skilled talent that new businesses need to survive and grow.”

Great post per usual. Let’s become the greatest entrepreneurial country we may want to believe we are.

> "The charge that policies like universal healthcare, paid family leave, and national childcare are “socialism,” or at least socialistic, stands in stark contrast to the importance of such policies to something quintessentially American and capitalistic — entrepreneurship."

Yes! A modest social safety net is a pro-business policy! The whole metaphor of it being a "safety net" implies it allows taking risks, like entrepreneurship or going back to school.

We'll have so many more entrepreneurs (especially from outside the wealthy, for whom quitting a job is less risky) if we introduce UBI and so many single person businesses deciding to finally employ someone else if they don't have to worry about health insurance because the government does