🤖⤴ The Age of AI and the Great Upshift: 2024 hopes

Hang on, it's going to be a bumpy ride!

Quote of the Issue

“The fall of Empire, gentlemen, is a massive thing, however, and not easily fought. It is dictated by a rising bureaucracy, a receding initiative, a freezing of caste, a damming of curiosity—a hundred other factors. It has been going on, as I have said, for centuries, and it is too majestic and massive a movement to stop.” - “Hari Seldon,” Foundation by Isaac Asimov

I have a new book out: The Conservative Futurist: How To Create the Sci-Fi World We Were Promised is currently available pretty much everywhere. I’m very excited about it! Let’s gooooo! ⏩🆙↗⤴📈

The Essay

🤖⤴ The Age of AI and the Great Upshift: 2024 hopes

After a boomy 1950s and 1960s, the US economy experienced the “Great Downshift in labor productivity growth — as described in my new book, The Conservative Futurist — resulting in economic growth far slower than what most experts in those immediate postwar decades had been predicting. Indeed, 2023 marks the 50th anniversary of the Great Downshift, which, in my analysis, began in the latter half of 1973, evidenced by consecutive quarters of declining productivity.

It would be quite fitting if this year, nearing its end, signified the beginning of a "Great Upshift." The second and third quarters saw some of the most substantial productivity growth in years. And while productivity stats are known for their volatile fluctuations, the timing of this increase alongside recent advancements in AI suggests the potential for a sustained improvement in productivity. This could lead to economic growth surpassing the current forecasts of many economists on Wall Street and in Washington. Instead of an economy barely able to generate 2 percent growth, maybe one able to manage 2.5 percent or even 3 percent. (Sotto voce: maybe even more.)

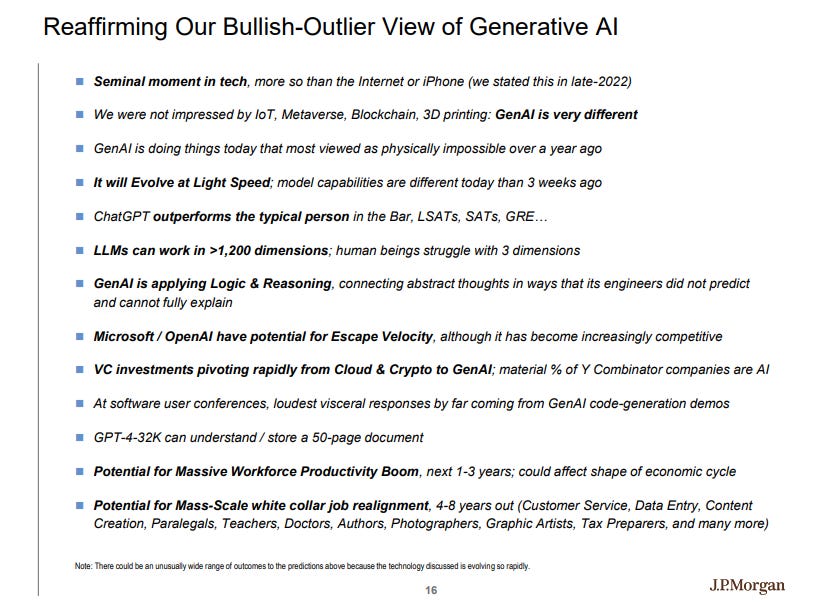

If we get a Great Upshift, it seems likely that American businesses investing in and productively using AI (generative AI, specifically, but machine learning broadly) would play a major role. A recent report from software analysts at JPMorgan (“Traction Control in Focus as GenAI Rubber Tries to Meet the Road”) certainly suggests some intriguing, even stunning possibilities:

So where do things stand heading into the new year? Here are some opinions I’ve gathering, including via Faster, Please! interviews, about the emerging Age of AI and how it could create a Great Upshift.

⏩ Marc Andreessen, a founder and general partner at Andreessen Horowitz (“My long read Q&A with Marc Andreessen on the importance of techno-optimism”):

The opportunity here is basically a step-function upgrade in human intelligence by basically joining the human and the machine in a symbiotic relationship. The opportunity is to take every drug developer and every creative artist of any kind, anybody trying to think through any kind of problem, and giving them a new kind of tool that they can work with that gives them a much greater chance of solving the problem or gives them the ability to solve problems we haven't even thought of yet. So this is potentially the big one. This is the big one that could basically drive everything else in the years and decades ahead.

⏩Erik Brynjolfsson, economist and director of Stanford Digital Economy Lab (“What to Expect in AI in 2024”):

I expect mass adoption by companies that will start delivering some of the productivity benefits that we've been hoping for for a long time. It's going to affect knowledge workers, people who have been largely spared by a lot of the computer revolution in the past 30 years. Creative workers, lawyers, finance professors and more are going to see their jobs change quite a bit this year. If we embrace it, it should be making our jobs better and allow us to do new things we couldn't have done before. Rarely will it completely automate any job — it's mostly going to be augmenting and extending what we can do.

⏩ Joseph Briggs and Devesh Kodnani at Goldman Sachs (“Upgrading Our Longer-Run Global Growth Forecasts to Reflect the Impact of Generative AI”):

First, if viewed as the “next wave” of technological innovation, the growth impact of generative AI may not be fully additive to the current GDP trend. Information and communication technology (ICT) has recently driven almost half of labor productivity growth in DM economies—reflecting both increased ICT investment and complementarities with existing inputs—so some AI-related gains may substitute for growth that would otherwise occur in a non-AI baseline.

Second, underlying productivity growth has slowed, with recent research suggesting that near-term total factor productivity grows linearly, with an occasional step-up following technological regime shifts, rather than exponentially. Unless AI ushers in a new productivity growth regime—an outcome that is possible but premature to forecast—the boost we anticipate from generative AI may be partially offset by an underlying growth slowdown.

In addition, barriers to adoption may delay productivity growth even if the full efficiency gains we see as possible are ultimately realized. Based on historical productivity gains following technological breakthroughs, commentary from business leaders, and cross-country technology adoption patterns, we anticipate that any GDP growth boost won’t exceed 0.1pp until 2027 in the US, 2028-2032 in other DMs and advanced EMs, and 2034 or later in other EMs.

Nevertheless, the enormous economic potential of generative AI suggests growth upside even after taking these offsets into account. In the coming weeks, we will therefore raise our growth forecasts in the second half of our ten-year forecast horizon as part of our 2024 outlooks, including by 0.4pp in the US, by 0.2-0.4pp in other DMs, and 0.1-0.2pp in advanced EMs by 2034.

⏩ Michael Feroli at JPMorgan (“2024 US Economic Outlook: Walk the line”):

When firms rapidly shed workers in 2020 productivity soared, in large part because it was mostly lower-skilled workers who were let go and lower-productivity sectors that shut down as a result of the pandemic. As firms re-staffed in the following years the opposite dynamic took hold, depressing productivity. … Productivity surprised favorably this year, and we think the trend may be drifting higher. However, for next year we project that cyclical developments will limit actual productivity growth to around 1.0%. However, we do think that trend productivity growth may be picking up from our prior estimate of 1.25% for the nonfarm business sector.

⏩ “Assessing the Implications of a Productivity Miracle” by analysts at Bridgewater Associates:

Forecasts about the development of AGI rest on highly speculative and untestable assumptions about how much more powerful models would need to become to develop humanlike intelligence. … [And] if we were to develop AGI, would it lead to explosive growth? Critics here point out that the testing and implementation of an AGI’s ideas would likely rely on processes that naturally take time or face resource constraints, like conducting experiments or sourcing and processing raw materials. Alongside potential obstacles from regulation or a lack of suitable training data for many tasks, these delays could prevent the rapid compounding that is necessary for explosive growth. Some say that super-advanced AI tools could just innovate their way out of these problems, but this claim is very challenging to assess from today’s vantage point. Given these considerations, full-blown explosive growth looks unlikely. But we wouldn’t rule it out at this early stage—and assigning it even a tiny probability would dramatically alter our average expectations for what the world will look like decades from now.

⏩ Matt Clancy and Tamay Besiroglu (“The Great Inflection? A Debate About AI and Explosive Growth”):

Besiroglu: Our second theme centers on the concept of “explosive growth.” I'm referring to a rate of growth that far surpasses anything we’ve previously witnessed — a minimum of tenfold the annual growth rate observed over the past century, sustained for at least a decade.

I am inclined to believe that such explosive growth is not just a possibility, but a probable outcome when we transition to an era where AI automates the vast majority of tasks currently performed by humans. To put this in numbers, I’d currently assign a 65% chance of this happening. I think you disagree with this view, correct?

Clancy: That’s right. While I think it’s very likely that growth will pick up once we deploy AI throughout the economy, I think it’s maybe a 10% to 20% chance, depending on how I’m feeling, that economic growth becomes explosive, by your definition, with most of that probability clustered around the low end of explosive growth.

⏩ Michael Strain, director of Economic Policy Studies at the American Enterprise Institute (“A Quick Q&A with … economist Michael Strain on the economic future of AI”):

There are a lot of serious people who think that this is going to be the most important technological advance in history since the printing press, something like that. That's not an unreasonable view.

I think it's going to be less impactful than that. I think we'll go back and say, “This was like the internet,” and, “That was a hugely transformative for daily life for the way we keep in touch with family and friends, for the way we communicate with professional colleagues and associates, with the way we shop, with the way we consume information.” Hugely transformative—probably not as transformative as electricity, indoor plumbing, advances in pharmaceuticals and medical treatments, these sorts of things, but it'll be an exciting couple of decades to see who's right about this.

⏩ Neil Shearing of Capital Economics (“AI, Economies and Markets”):

Generative artificial intelligence (AI) would appear to have all the characteristics of a “general-purpose technology” that will revolutionise economies and has the potential to deliver a substantial boost to productivity growth. … Our proprietary AI Economic Impact Index, which ranks countries according to their ability to innovate, adopt and adapt to AI, suggests that the US will lead the AI revolution. Along with beneficiaries including Singapore and South Korea, US productivity growth will accelerate to over 2% a year in the 2030s. … One consequence of the AI revolution is therefore likely to be greater US economic outperformance of Europe. … China will lead some aspects of the AI revolution but will struggle in others. This is in part because AI is likely to become a new fault line in global economic fracturing, which will reduce China’s access to US technology and mean it will need to develop AI capabilities domestically. Moreover, while we expect AI to boost productivity growth in China, this will be more than offset by structural headwinds pushing in the other direction. A combination of weaker growth in China and the boost to US productivity from AI means that we expect the US to remain the world’s largest economy over the coming decades.

⏩ Mark Zandi of Moody’s Analytics (“U.S. Retrospective and Outlook”):

Worker productivity growth has also bounced back to more than 2% year over year. The reasons are difficult to pinpoint, but given all the job switching during the pandemic workers are happier and more productive in jobs better suited to their skills and education. Remote work and the related surge in investment in information processing equipment and software early on in the pandemic are also likely contributing. Artificial intelligence is sure to boost productivity, but that is still very much a forecast. This supply-side revival allows the economy to grow more quickly without fanning inflation. … It would also be sensible to expect labor productivity growth to return to the 1.5% per annum underlying pace that has prevailed since prior to the pandemic. This would put the economy’s potential growth—the rate consistent with stable unemployment—at no more than 2% per annum. This is consistent with our forecast of 1.7% real GDP in 2024 and a small increase in unemployment to just over 4%.

⏩ Julia Coronado of MacroPolicy Perspectives (Financial Times op-ed):

The surge in longer-term bond yields that started this past summer came first and foremost as the US economy proved more resilient than expected while inflation cooled notably faster than anticipated. This was in direct contradiction to the macro narrative that a recession would be required to bring inflation down. This outcome stems from the reappearance of the holy grail of economics — productivity gains. … Some of the bounce-back can be traced to recovering global supply chain operations. Pandemic-related frictions were a major source of sand in the gears of business operations in 2021 and 2022 and inflation in consumer and industrial goods prices.

This source of productivity improvement could be short-lived, since recovering supply chains won’t continue to lower unit production costs. The real question is whether productivity can continue to grow at a healthy pace. There are two reasons to think the productivity performance could improve on the lackluster performance following the financial crisis of 2008-9. The first has to do with the sizzling hot labor market recovery. Record amounts of people quit their jobs in the past few years. This was a challenge for companies but quit rates have come back down toward pre-pandemic levels which can provide a near-term boost to productivity as the costs of hiring and training new workers comes down. The churn of workers in recent years could also pay longer term dividends as it may mean that workers are matched up with employers who are a better fit.

Another byproduct of a hot labor market — as well as the unique operational challenges of the pandemic — is that we had the first recession without an extended fall in business investment, a hallmark of most downturns. Businesses kept investing in equipment and intellectual property at a historically high rate to meet the needs of remote work, as well as offset some of the need for workers amid a very tight labor market. The technological tools companies have at their disposal to re-engineer business processes and realize efficiencies have arguably never been more abundant. If they realize anything close to a historical average return on investments made over the past few years, we may very well be in for a better productivity trend this cycle.

Looking back a year from now, I hope that even the most bullish opinions will have proven to be too cautious.