⏰ Russia Invades Ukraine: Will a Warring ‘20s Prevent a New Roaring ‘20s?

Also: 5 Quick Questions for … author Sebastian Mallaby on venture capital

In This Issue

The Essay: Russia invades Ukraine: Will a Warring ‘20s prevent a New Roaring ‘20s?

5QQ: Five Quick Questions for … author Sebastian Mallaby on venture capital

Micro Reads: Inflation, robots, flying cars, and more …

Nano Reads

Quote of the Issue

“If we don’t end war, war will end us.” - H.G. Wells

💥 Important Update for My Wonderful Faster, Please! Readers and Subscribers

I currently intend to start offering a paid subscription option to Faster, Please! as of February 28 — the very next issue! While I’m still working out the exact details, accessing my twice-weekly essays and Q&A interviews with top thinkers (along with some surprises) would be included in that paid subscription, but not the freebie version. I have been writing this newsletter over the past year at night and on weekends. I hope you find it valuable.

My friends: I still believe we’re at the start of an amazing period of American (and world) history — the beginning of a Great Acceleration in human progress. It’s the purpose of Faster, Please! both to document these steps/leaps forward and recommend the best ideas to make sure they happen, ASAP. You know, faster, please! I look forward to taking that journey — via economics, tech, public policy, business, history, culture, and a smidgen of politics — over the next months and years with all of you. Let’s make a better world for everyone, together. Melior mundus

The Essay

⏰ Russia invades Ukraine: Will a Warring ‘20s prevent a New Roaring ‘20s?

I read a lot of Wall Street research, and I’ve been getting little sense of any deep concern about the longer-term impact of Russia’s dastardly attack on Ukraine, at least not yet. Lots of focus on near-term commodity prices and the impact of monetary policy.

This from Goldman Sachs is typical:

Any direct effects on the US economy should be limited because trade links are weak and energy prices are likely to be affected far less in the US than in Europe. … The growth hit could be somewhat larger if geopolitical risk tightens financial conditions materially and increases uncertainty for businesses. … With some signs of problematic wage-price dynamics emerging and near-term inflation expectations already high, further increases in commodity prices might be more worrisome than usual. As a result, we do not expect geopolitical risk to stop the FOMC from hiking steadily by 25bp at its upcoming meetings, though we do think that geopolitical uncertainty further lowers the odds of a 50bp hike in March.

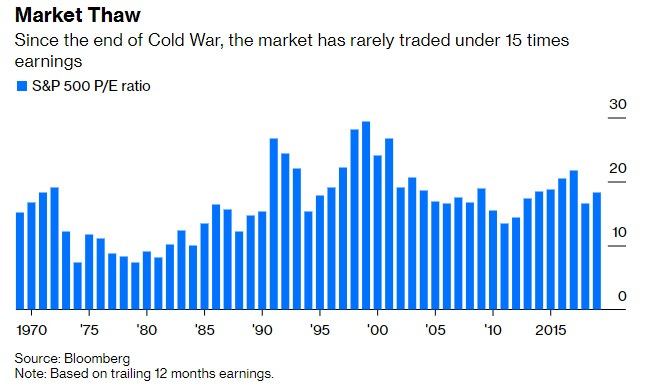

But it’s not hard to imagine a more serious economic impact if this war doesn’t stay contained to the Ukraine, as bad as the conflict there already is. The US annually exports nearly half a trillion dollars in goods and services to the European Union and its $15 trillion economy. And if you pull the camera back, you’ll still see the potential for even more economic damage over the longer term. Let me again highlight this chart of the price-earnings ratio of the S&P 500, based on trailing 12-month earnings.

The chart comes from a 2019 Bloomberg column by Stephen Gandel that highlights the work of Nobel laureate economist Robert Shiller in noting that from 1871 through 1990, the average P/E of the stock market was 13.6 and rarely rose above 18. Then something changed. Starting in 1991, the market’s P/E multiple took off. Since then, Gandel continues, it’s rarely been below 18, averaging 23 in the 1990s and 19.5 in the 2000s. It’s currently at 23 or so. As Grandel explains:

Many factors probably contributed to the market’s valuation shift, but one of the most frequently cited is the so-called peace dividend. The Berlin Wall fell, the Soviet Union collapsed in late 1991, and stocks took off. It’s hard to quantify just how much of a boost came from the downfall of a military superpower and the reduced threat of nuclear war. … But a big lift undoubtedly came from a reshuffling of the world order with the United States firmly on top.

What emerged from the collapse of the Soviet Union was a New World Order, a unipolar one dominated by a global hyperpower, the United States. And that American dominance cemented and maintained a global, rules-based system where there was no realistic alternative to market capitalism. But now a reversal, and we’re getting a glimpse of the Old World Disorder with war in Europe perhaps to be followed by war in the South China Sea. We’ll see to what extent Mr. Market agrees that there’s a risky New Geopolitical Normal now in play.

The bull case for a New Roaring Twenties endures, pretty much

So: What of my hopes for a boomy New Roaring Twenties of accelerated economic and productivity growth? There is a bull case here. Most importantly, the innovation cycle being driven by AI, as well as advances in biotechnology, energy, and space, does have its own momentum. For example: As I wrote last issue, there’s growing evidence of the diffusion of machine learning throughout the economy. And the money pouring, for instance, into nuclear fusion startups seems unlikely to abate. Indeed, this conflict may well hasten the growing rethink about nuclear power in Europe and America. Also, I’m pretty sure Elon Musk is going to keep launching those rockets.

Then there’s this: It often takes an emergency or threat for America to do some important long-term things. World War Two led to the GI Bill bill and the Interstate highway system, while the Cold War led to Apollo and the internet. It’s an analysis one also finds in the 1998 film Armageddon when the American president addresses the world: “For the first time in the history of the planet, a species has the technology to prevent its own extinction. … The human thirst for excellence, knowledge, every step up the ladder of science, every adventurous reach into space, all of our combined modern technologies and imaginations, even the wars that we've fought have provided us the tools to wage this terrible battle.”

(If you’re looking for a deeper analysis of this point, let me suggest the 2014 book War! What Is It Good For?: Conflict and the Progress of Civilization from Primates to Robots by historian Ian Morris, which argues that war needs have led societies to create larger and more organized societies, including the ability to borrow and tax.)

Perhaps the prospect of a dangerous world will not only result in bigger defense budgets, but also more of a focus on making long-term changes — including R&D investment and deregulation — to keep the US economically sound and pushing forward the technological frontier. Indeed, the Chinese geopolitical threat is already being used as an excuse to do or not do things in Congress, from immigration to Big Tech antitrust.

But if you’re going to worry, this is what you should worry about

Unfortunately, I think there’s a bear case, too. Greater policy uncertainty could lead to less business investment, critical for faster productivity growth. Maybe more government R&D funding, sure — but perhaps directed toward obviously military applications rather than civilian ones. Think about what happened during World War Two. In his book The Rise and Fall of American Growth, Northwestern University economist Robert Gordon argues that there was a great leap forward in total factor productivity — a way of measuring the productivity impact of innovation — during the war. Gordon writes

Production miracles during 1941– 45 taught firms and workers how to operate more efficiently, and the lessons of the wartime production miracle were not lost after the war: productivity continued to increase from 1945 to 1950. In addition to the increased efficiency of existing plant and equipment, the federal government financed an entire new part of the manufacturing sector, with newly built plants and newly purchased productive equipment.

Gordon himself concedes the surprising nature of his finding. And other economists have taken issue with it. In the paper The Rise and Fall of American Growth: Exploring the Numbers, University of Warwick economists Nicholas Crafts fails to finds a TFP surge during the war. He also notes a big decline in new technology publications — “a valuable indicator of the production of useful new technical knowledge” — during World War II and its aftermath. His conclusion, which gets at my concern:

It seems probable that World War II diverted research effort and learning away from commercially relevant activities). The 1930s and 1940s saw significant changes to several aspects of supply-side policy that matter according to endogenous-growth economics including research and development (R&D), infrastructure, taxation, and regulation. On balance, it seems quite likely that these had adverse effects on TFP growth by reducing the rate of return to innovative effort.

(A version of this distraction argument gets played out in the book and television series The Expanse where efforts by the citizens of an independent Mars to terraform the Red Planet get delayed as they are forced to divert resources into military defense for their Cold War with Earth.)

And, of course, heaven forbid, military conflict expands both on Earth and in a militarized space. Finally, the super bear case would be any sort of nuclear conflict. From the 2012 paper “The Economic and Policy Consequences of Catastrophes” by Robert S. Pindyck (MIT Sloan School of Management) and Neng Wang (Columbia Business School):

Various studies have assessed the likelihood and impact of the detonation of one or several nuclear weapons (with the yield of the Hiroshima bomb) in major cities. At the high end, Allison (2004) put the probability of this occurring in the next ten years at about 50%! Others put the probability for the next ten years at 1 to 5%. . . . What would be the impact? Possibly a million or more deaths. But the main shock to the capital stock and GDP would be a reduction in trade and economic activity worldwide, as vast resources would have to be devoted to averting further events.

Bottom line: I tend to side with the bull case. That said, my big concern right now isn’t with economics but with the welfare of the Ukrainian people and their democracy.

5QQ

❓❓❓❓❓ Five Quick Questions for … author Sebastian Mallaby on venture capital

Sebastian Mallaby is the Paul A. Volcker senior fellow for international economics at the Council on Foreign Relations. The author of five books, including More Money Than God: Hedge Funds and the Making of a New Elite and The Man Who Knew: The Life and Times of Alan Greenspan, his latest is The Power Law: Venture Capital and the Making of the New Future, released earlier this month. (You can check out my recent podcast chat with him here. This fresh Q&A expands upon that conversation.)

![The Power Law: Venture Capital and the Making of the New Future by [Sebastian Mallaby]](https://substackcdn.com/image/fetch/$s_!UChf!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F067b6871-2170-47fc-8ca9-716128aa5601_228x346.jpeg "The Power Law: Venture Capital and the Making of the New Future by [Sebastian Mallaby]")

1/ There’s an argument that Silicon Valley venture capitalists have been engaged in the trivial. It's the "No flying cars, but we did get Twitter" argument. Is there something to that?

This is nonsense. Venture capital does a ton of different things. It funds food tech: in other words, meatless hamburgers like Impossible Foods. It funds new kinds of nuclear power. It funds e-batteries. It funds SpaceX. Sure, there's plenty of software because we're in a phase where software is eating the world, but it's not restricted to software.

2/ Do you think that policymakers in the United States have drawn the wrong lesson from the rise of China? Some see China focusing on certain technologies and making advances and they think, "Well, the key is for us to do the same thing in our own way."

The idea that China's industrial policy built the digital economy is wrong. There was an industrial policy around tech in the late 1990s in China. It was focused on building a semiconductor industry. We know today that failed totally. They are still trying to build a semiconductor industry. Meanwhile, the government ignored consumer-facing technologies. So private venture capitalists, in fact, private venture capitalists from the United States, moved in and funded all the early, consumer-facing digital economies in China, from Baidu to Alibaba to Tencent. And the government was looking the other way. It's a perfect illustration of how, in fact, industrial policy is not the right way to build a digital economy.

3/ Do we get overly excited when we see VC money pouring into an emerging sector? I think of the nuclear fusion sector. We think, "Wow, now it has passed the market test. It must be real." Do we draw that conclusion too easily and underestimate how risky these bets are?

Yes, we do. Venture capitalists frequently spot the emerging trend, which is not actually the emerging trend. There have been waves of excitement about all kinds of things that went nowhere. Often they end up going somewhere 10 years later when the technology advances enough to actually build the thing that they were trying to build before. But it's very easy for large amounts of venture money to be wasted. That's part of the game. That's why my book is called The Power Law.

4/ Why is Europe's entrepreneurial ecosystem less vibrant than America's?

People wrongly claim that Europe is fundamentally risk averse. The reason it has been risk averse is that there weren't enough venture capitalists to underwrite the risk. If nobody is there to provide the capital for somebody to do a startup, they won't do the startup. If nobody is there to reassure the first five engineers who join the startup that they'll get another job if it fails, then those five engineers are not going to join the startup. What's changing now is venture capital is flooding into Europe. I predict that Europe's risk appetite will all of a sudden materialize.

5/ Do you have a favorite VC story of a funding that didn’t seem like it was going to work, but of course they got it right and it worked?

A great classic story of VC funding is Cisco, the go-to router company that dominated computer communications from the late '80s through the early 2000s. This was a case where the startup was so chaotic that people would have fistfights in the office. It was so penurious that it was in an area of Palo Alto where it was not uncommon for bullets to be fired at the building. And the founders were, shall we say, chaotic. The venture investor came in, installed not only a chief executive, but a head of engineering and hired every single senior person that the company needed and eventually fired the founders. And out of this totally improbable shell, created a company that became a pillar of Silicon Valley.

⭐ Bonus: Do you have any sense of what the founders and technologists in Silicon Valley make of Elon Musk? Greatest entrepreneur or greatest showman?

I think at this point, it's hard to dismiss him as just a showman. Clearly he is a showman, but that's actually part of being a good entrepreneur, because you do have to tell a story that paints where you're trying to get to and inspire people to believe in that vision. So showmanship is all part of the game. But somebody who has built Tesla, which has fundamentally forced the global car industry to reevaluate the potential of electric cars, and somebody who has built SpaceX, which has forced incumbents like NASA to fundamentally reevaluate how you do space launches and how cheaply you can do them — those are two epic achievements. To have done one of them would be fabulous. To do both of them is just like fabulous squared. So I think the Valley totally respects Elon.

Micro Reads

🔥 Will Inflation Moderate as Pandemic Fades? Mark Zandi, Moody’s Analytics |

The outlook for the economic recovery hinges on the prospects for inflation. If inflation moderates as the pandemic fades, then the recovery will evolve into a self-sustaining economic expansion. This is the most likely scenario. However, if the high inflation persists, either because the pandemic intensifies, further disrupting supply chains and labor markets, or because inflation expectations become unanchored and precipitate a negative self-reinforcing wage-price spiral, then the Federal Reserve will have no choice but to tighten monetary policy more aggressively. The recovery may very well unravel into recession. The odds of this dark alternative scenario are still low, but they are rising.

🤖 Covid has reset relations between people and robots - The Economist | Advances in AI, paired with the social and economic changes of COVID-19, are accelerating the spread of robots in the economy. With the current labor force participation slump, robots are taking over many mind-numbing, repetitive, and physically demanding jobs humans don't want and machines are well-suited to. Robots stand to deliver economic gains, but regulations are inhibiting their entrance into sectors like medicine and autonomous delivery.

🚁 Electric Flying Cars Are Just Dirty Old Helicopters, Rebranded - David Fickling, Bloomberg | With more than $12 billion in investment since 2010, electric vertical takeoff and landing aircraft, or eVTOLs, are generating buzz as the flying cars we've been promised. But are these personal aircraft more clever marketing than engineering marvel? With emissions no better than traditional gasoline cars for short trips, these flying cars aren't the climate solutions they've been presented as. Beyond carbon emissions, noise pollution may be another reason to temper our excitement. eVTOLs promise to produce only fractions of the decibels helicopters do, but quieter doesn't always mean less annoying, and the incessant insect-like buzz of having these aircraft zipping around our cities is sure to evoke some NIMBYism in all of us.

🚀 Star wars: why Nasa objects to Elon Musk’s space race - Peggy Hollinger, Financial Times | NASA has joined SpaceX's rivals in voicing concerns about the Elon Musk-founded rocket company's plans to launch 30,000 more satellites into low-Earth orbit for its Starlink internet service. In a letter to the FCC, NASA argued that SpaceX's satellite network could contribute to space debris and make predicting asteroid strikes on Earth more difficult. SpaceX insists that its autonomous satellites can evade collisions and aims to reduce interference with Earth-based astronomical observation. Still, NASA would like SpaceX to demonstrate its technology on these fronts.

Nano Reads

▶ 2022: 10 Breakthrough Technologies - MIT Tech Review

▶ China Plans Asteroid Missions, Space Telescopes and a Moon Base - Elizabeth Gibney, Nature |

▶ GM seeks US approval to deploy self-driving car without a steering wheel - Jon Brodkin, Ars Technica |

▶ What would a thriving progress movement look like? - The Roots of Progress |