Why Tesla's $1 trillion valuation says something good about the US economy

Why Tesla's $1 trillion valuation says something good about the US economy

Also: America: A zero-risk society that ignores the future

“The great difference between Young America and Old Fogy, is the result of Discoveries, Inventions, and Improvements. These, in turn, are the result of observation, reflection and experiment.” - Abraham Lincoln, Lecture on Discoveries and Inventions

In This Issue

The Micro Reads: Space economy, geoengineering, Bitcoin, and more . . .

The Short Read: Will Tesla be the first $3 trillion company?

The Long Read: America: A zero-risk society that ignores the future

The Micro Reads

🚀 Jeff Bezos’ Blue Origin plans ‘business park’ in space - Financial Times | “According to a promotional website, the station, to be called Orbital Reef, will be an ideal location for a ‘space hotel’, ‘film-making in microgravity’ or ‘conducting cutting edge research’. Those on board would experience 32 sunsets and sunrises each day, the company said. The modules for Orbital Reef will be launched into space via Blue Origin’s reusable New Glenn rocket, which has been beset by repeated delays.” Not long ago, I did an AEI event that included executives from Sierra Space and Redwire, two of the companies involved in this effort. Here’s a transcript.

⛓ Blockchain Analysis of the Bitcoin Market - Igor Makarov & Antoinette Schoar, NBER | This is a detailed analysis of the Bitcoin network and its participants. So much fascinating info here: “The individual holdings are still highly concentrated: the top 1000 investors control about 3 million BTC and the top 10,000 investors own around 5 million bitcoins.”

⚛ Nuclear Fusion Edges Toward the Mainstream - New York Times | “Why put money into a far-out quest that has never made a nickel? Investors say they are attracted to the prospect of an early entry into a potentially game-changing technology: a fusion reactor that produces far more energy than goes into it. Such an achievement could have enormous commercial promise.”

🌤 What is geoengineering—and why should you care? - MIT Technology Review | A good explainer on both the history of geoengineering as well as the pros and cons. And I think the kicker is spot-on: “As those [climate] effects worsen, the public and politicians may come to think that tinkering with the entire planet’s atmosphere is a risk worth taking.”

⚡ All manner of industries are piling into the hydrogen rush - The Economist | “Hydrogen is expected to play a big role in greening hard-to-decarbonise sectors such as cement and steel, as well as in long-term energy storage. Today’s smallish and, because almost all the stuff is made from fossil fuels in a carbon-intensive way, dirtyish hydrogen business is forecast to grow into a much cleaner trillion-dollar industry in a few decades. Governments are spending tens of billions of dollars a year to kickstart a clean-hydrogen revolution. A posse of hydrogen-curious firms are keen for a piece of the action.”

🌋 Geothermal energy as a climate solution - Political Economy podcast with Jamie Beard | I recently chatted (transcript) with Jamie Beard, founder and executive director of the Geothermal Entrepreneurship Organization at the University of Texas at Austin. One interesting quote from Beard: “I think we have a narrow window to get oil and gas excited about doing this. If we miss that window, and oil and gas decides to pivot into solar and wind and hydrogen and doesn’t really pay much attention to geothermal, geothermal is never going to scale fast enough to be competitive with solar and wind.”

📱 Tweetstorm of the Issue:

The Short Read

🚘 Will Tesla be the first $3 trillion company?

Tesla crossed $1 trillion in market value on Monday, thanks to an order for 100,000 cars from rental-company Hertz. (The surging stock also pushed the personal wealth of founder Elon Musk, the world’s richest person, close to $300 billion.) Its value has increased fivefold since July 2020 when it overtook Toyota to become the world’s most valuable carmaker, with the company now worth more than the next nine most valuable public automakers combined, notes the Financial Times.

Tesla’s achievement sparked my recollection of a 2013 Saturday Night Live sketch where a bunch of American gadget geeks are forced to make their complaints about the new iPhone 5 in front of the poor Chinese workers who assembled the devices. It concludes with the workers given an opportunity to complain about American-made products. One worker (played by Fred Armisen ) sarcastically responds, “Let’s see: Does diabetes count as a product? If not, we’ll have to get back to you.”

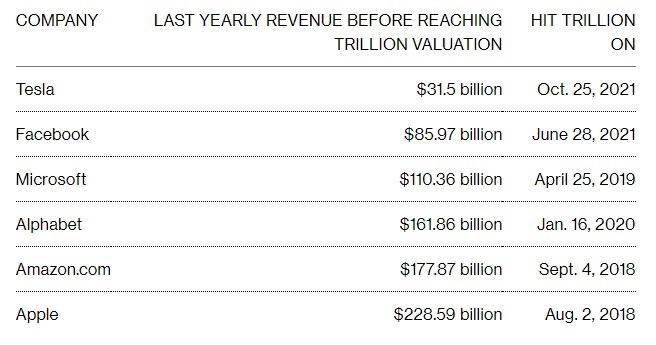

The audience roared. Of course they did. Everyone knows America doesn’t make anything anymore. But, you know, Tesla does. And what it makes investors apparently think is pretty valuable, both now and in the future. Indeed, they think the potential of what Tesla makes is so valuable that no company has itself become so valuable despite selling so little, as this graphic from Bloomberg points out:

Also, don’t forget Musk’s SpaceX, whose reusable launch technology is helping the long-time dream of a space economy take a giant leap forward. (“If you think commercial space is getting exciting now . . . just wait until the SpaceX Starship starts flying. It's a 100% reusable rocket designed to launch over 100 tons or 100 people to space at one time and will dramatically reduce the cost of getting to space!” tweets astronaut and NASA veteran Garrett Reisman.) And SpaceX is hardly alone in this effort. Amazon founder Jeff Bezos’ space exploration company Blue Origin just announced plans to launch a commercial space station — “a mixed-use business park” — into low-earth orbit by the late 2020s. Meanwhile, Amazon remains a logistics marvel whose cloud computing business is a pretty important bit of American digital infrastructure.

The economics of the SNL sketch were perhaps most screwy when it came to Apple. Most of the value of the iPhone — arguably the most successful consumer product of all time — derives from its design of the hardware and the technological capabilities of its operating system, not its underlying parts or their assembly. The salaries of Chinese workers who assemble Apple iPhones start at around $300 a month. And if SNL writers think Apple is a joke company that doesn’t make anything, then their opinion of Google and Facebook is probably far worse.

It makes sense that the Information Technology Revolution would make lots of fortunes through the manipulation of bits. But maybe now we are shifting back to wealth creations via the manipulation of atoms — enabled, of course, by IT advances, including forms of AI — rather than our attention spans via social media. Tesla is one example, and more might be on the way. For example: Moderna is a $140 billion company thanks to its success developing mRNA vaccines to counter the coronavirus. One wonders about the economic potential of new genetic editing techniques.

Or how about energy? A recent online poll asked what would be the first $3 trillion company. Apple was the obvious answer since it’s already two-thirds of the way there. Tesla also got a few votes. The bull case can be found in a Bloomberg quote of a Tesla analyst: “Wall Street is starting to believe the skyrocketing move with Tesla’s stock price is nowhere near over since Tesla has a massive lead in the EV space and improving growth potential as the U.S., European and Asian markets for electric cars grows.”

But I like the optimism of folks who picked Commonwealth Fusion Systems, a company aiming to build a compact thermonuclear fusion reactor. Or maybe it will be a geothermal company or, perhaps, an existing oil and gas company that pivots to geothermal.

Biology, energy, space. The US economy is about a lot more than tech firms serving us ads while we search online or while we bicker on social media platforms. Will it all add up to the start of a New Roaring Twenties or Roaring Twenty-First Century? I’ll have to get back to you.

The Long Read

📉 America: A zero-risk society that ignores the future

Do we live in a zero-risk society? That’s the claim made in the 2020 paper “Are ‘Flows of Ideas and ‘Research Productivity in secular decline?” by Peter Cauwels and Didier Sornette at ETH Zurich. In the previous issue of Faster, Please!, I explored the paper’s topline conclusion: “Our main result is that scientific knowledge has been in clear secular decline since the early 1970s for the Flow of Ideas and since the early 1950s for the Research Productivity.” In other words, there’s been too much “innovation and exploitation of existing knowledge” and too little “discovery and invention, or new explorations.”

The Cauwels-Sornette finding is most obviously supported by the long-term downshift in US productivity growth. One can also see it in the analysis of the late innovation guru Clayton Christensen, who argued the US economy was generating many fewer game-changing “empowering innovations” — think the Ford Model T or the personal computers of IBM and Compaq — than in the past. I would also point to the work of economist Daron Acemoglu, who has written about the risk that too much innovation has been, and will continue to be, of the sort that automates existing tasks rather than creating new, complex tasks.

So what has caused this supposed “clear, secular decline” in scientific knowledge? Although big scientific advances might well be getting harder to find (requiring more researchers and resources), Cauwels and Sornette don’t think we’ve somehow reached the end of science. Rather, they see the decline as a consequence of our “zero-risk society,” which itself is the result of five deeper causes:

First of all, it is the direct consequence of economic progress itself. When wealth and age in society increases, people become ever more risk averse, focus on going concern, protection of existing wealth and rent seeking. This, however, mainly applies to the well-to-do, which brings us to our second argument. To be able to take risks, it is necessary to be empowered and have access to opportunity. As inequality in the affluent society has been soaring in recent decades, a growing proportion of citizens in many western countries (not to speak of developing countries) struggle to get through their daily lives, suffer poor health, have no access to high-quality education or a decent social security safety net. Thus, they already experience risky lives, but here only with downside risks as opposed to the upside risks associated with innovation and entrepreneurship that we advocate here. Third, technological advance creates an ‘illusion of control’. We have the cozy feeling of being protected and secure and that technology will save us from any harm or adverse events. Fourth, this is all amplified by herding and imitation through social media, where, fifth, often, over-reaction occurs, which leads to a management by extremes. Through the instinctive reaction of our reptilian brain and the availability bias provided by social media and the media as merchants of attention, the probability of rare events tends to be often enormously overestimated. When policy makers give in to this tendency, they yield to populism. Furthermore, we often only fight symptoms, superficially, without looking for deeper root causes of the problems that our society is facing.

I think that interesting explanation misses or downplays a few things, including the rise of anti-growth environmentalism (although that’s an outgrowth of economic progress) and the harmful feedback loop it created between policy and culture, as well as the macro-factors making progress harder (such as the full exploitation of the “great inventions” of the past, as documented by Northwestern University economist Robert Gordon). But to back to my original question: Do we really live in a “zero-risk society?” I think there’s other evidence in addition to the “secular decline in scientific knowledge.” For example:

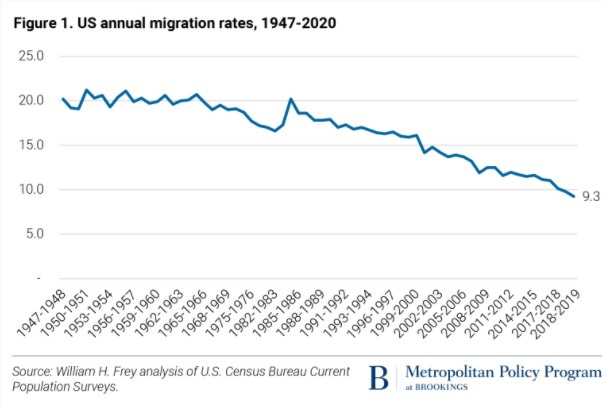

Americans don’t move as much as they used to.

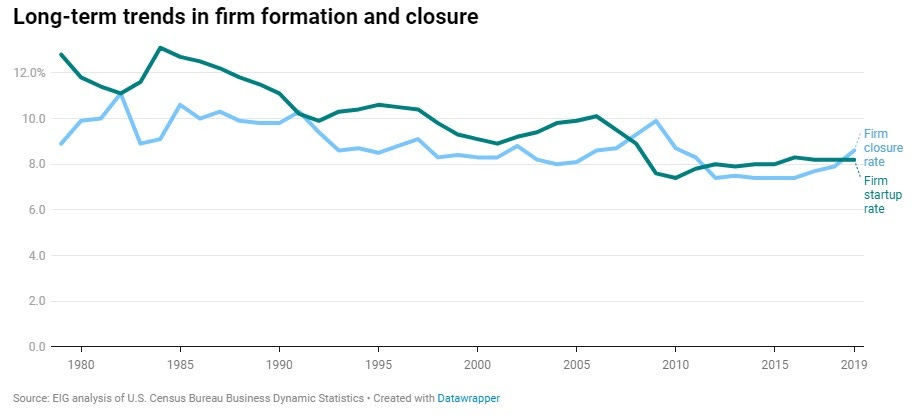

Americans don’t start businesses the way they used to.

Americans don’t own stocks the way they used to.

Of course, all of the above items carry context that could justify a separate essay for each. And perhaps the pandemic, rather than making us more risk-averse, will cause just the opposite effect. In my recent podcast chat with economist John Haltiwanger of the University of Maryland, the entrepreneurship expert talked about the surge in startups beginning in the summer of 2020, although he suspects the sorts of businesses started last summer were different — perhaps less out of necessity given the recovering job market.

Haltiwanger: “So the question is whether the businesses that started last summer were the necessity/transitory kind that took advantage of the fact that there were lots of pandemic-related needs in the economy, and whether the businesses this spring are a little bit more forward-looking and will maybe even persist a little longer. We don’t have any evidence to determine the answer at this point.”

One final data point about the zero-risk society comes from Mass Flourishing by Nobel laureate economist Edmund Phelps:

In Lost in Transition, Christian Smith finds evidence from his interviews with young adults that they have not found their way. Their difficulties arise not from any failure of their own but from society’s failure to provide them the cultural resources to help them in their journey to adulthood and help them thrive. Asked about the consumerism around them, most are positive— some justifying it as good for the economy. Asked to talk about what sort of a life they would like to lead, they speak about working for the money— working to have “nice things,” a family, and financial security. Very few spoke of the nature of the work they wanted to do. The words “challenge,” “exploration,” “adventure,” and “passion” were not in their vocabulary. They are lost.

The zero-risk society thesis dovetails nicely with the notion that America has become a less “future-oriented society.” One of my favorite studies is one by Yale University economist Ray Fair that highlights a steady decline in US infrastructure spending as a percent of GDP beginning in 1970. And right around the same time, the federal government started running big budget deficits. Fair argues the two occurrences reflect a sustained change in national attitude: “The overall results suggest that the United States became less future oriented beginning around 1970. This change has persisted.” The logic here is simple: Fixing your roof while the sun is shining and curbing spending before the bill collector calls require some foresight and the ability to place the current you in the shoes of future you.

I could also point to our culture as a problem from either the zero-risk or future-orientation perspective. Cauwels and Sornette: “Why not promote the risk-taker, the explorer, the creative inventor as a new type of social influencer acclaimed like a Hollywood or sports star?” And Phelps: “But what a modern economy needs more than personnel with expository skills is people eager to exercise their creativity and venturesome spirit in ever-new and challenging environments. It needs people who when they were young read the intriguing and uplifting works of the imagination by the likes of Jack London, H. Rider Haggard, Jules Verne, Willa Cather, Laura Ingalls Wilder, Arthur Conan Doyle, and H. P. Lovecraft.”

One of my favorite documentaries is Civilization, the 1969 BBC mini-series written and narrated by British art historian Kenneth Clark. Over 13 episodes, Clark presents the history of the West through its art. It was Clark’s goal to make manifest the famous quote — cited in the series — of 19th century English art critic John Ruskin: “Great nations write their autobiographies in three manuscripts, the Book of their Deeds, the Book of their Words and the Book of their Art. Not one of these books can be understood unless we read the two others, but of the three the only trustworthy one is the last.”

What does our Book of Art say about modern American society? What do our films, television shows, books, video games, even our memes say about this great nation? My answer to that question is a frequent subject of this Substack.

2 of the reasons for our decline in risk taking seem to be in conflict. If increased wealth dampens our appetite for risk, why wouldn’t a more extensive safety net do the same?