📈 What is the outlook for long-term US economic growth?

Worrisome. But those trends aren't immune to our actions. Policy matters. Our decisions matter.

Quote of the Issue

“Once you start thinking about growth, it's hard to think about anything else.” - Nobel laureate Robert Lucas

The Essay

📈 What is the outlook for long-term US economic growth?

Financial markets and financial journalists were intently focused on Federal Reserve Chair Jerome Powell’s speech at the recent Jackson Hole policy symposium. I was, too, of course. But I was also greatly interested in what Charles Jones, an economist at Stanford University’s business school, presented there about the future growth prospects of the American economy. (BTW, he’s mentioned in the preface of my upcoming book, 🚀 The Conservative Futurist: How to Create the Sci-Fi World We Were Promised, out October 3 and available for pre-order right now.) Jones has written or co-authored some of my favorite papers on the subject of growth. Among them:

"The Past and Future of Economic Growth: A Semi-Endogenous Perspective"

"The End of Economic Growth? Unintended Consequences of a Declining Population"

At the annual conference in Wyoming, Jones contributed “The Outlook for Long-Term Economic Growth” (including a great slide deck, from which I have plucked a few relevant images). Here are some of the most important takeaways:

➡ To forecast the future, start by understanding the past. The US has experienced an eventful economic history over the past 150 years, plenty of booms and busts — and one notable mega-bust. Yet the broad growth in American living standards has exhibited a surprising statistical regularity over the long run. That overall steadiness can be seen in the following chart where a straight line with a slope of 2 percent annually fits nicely with the logarithm of inflation-adjusted US per capita GDP — although Jones warns readers to be “cautious about assuming this continuation.” Oh, I’m aware — and I will!

➡ Growth is powered by ideas. Lots of them. Living standards tend to rise over time because of the accumulation of ideas. Unlike most goods, such as computers or oil, ideas can be used by many people at once without being depleted, Jones explains. (The fancy economic concept here is that ideas are nonrival or “infinitely usable,” as he puts it.) For example: The COVID-19 vaccine can benefit billions of people once it is invented. The total number of ideas ever discovered depends on the number of people searching for them, such as researchers and entrepreneurs.

Growth is made up of people, my fellow humans! Therefore, Jones explains, income per person (or our living standards) is linked to the number of people looking for ideas. (“Income per person ← Ideas ← People”) As such, the growth rate of income per person is limited by the population growth rate of the countries that produce ideas. (“Growth in income per person ← Growth in people searching for ideas”)

➡ There are five headwinds that might slow growth in the US and other rich countries.

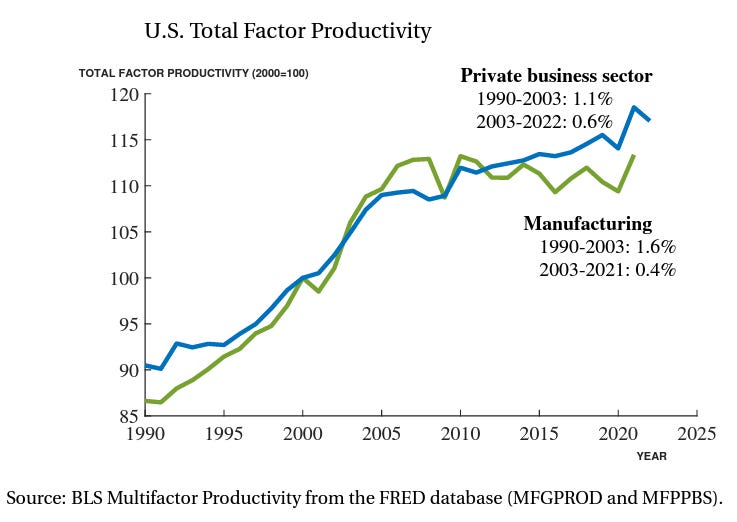

First, “growth is already slowing.” Total factor productivity — a measure of an economy’s efficiency and innovativeness — has slowed in the US since 2003. Full stop — and notably that decline precedes the Global Financial Crisis.

Second, “ideas are getting harder to find.” Jones points to Moore’s Law, the doubling of computer chip density every two years, as an example of how more and more researchers are needed to sustain constant innovation. He also observes that the growth rate of research employment has declined in many countries since 2002, which may contribute to the slowdown in productivity growth. Remember: “Growth in income per person ← Growth in people searching for ideas.”

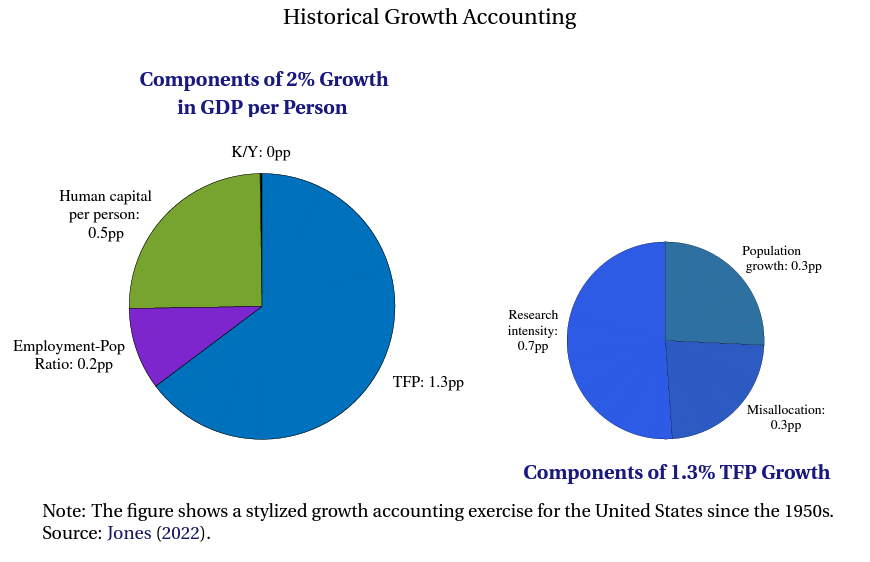

Third, investment rates in “infinitely usable ideas” can’t rise forever. The US has been investing more and more of its GDP in intellectual property products — such as privately funded R&D, publicly funded R&D, and computer software — which are non-rivalrous ideas that can boost productivity and growth. Jones: “This investment rate in ideas has risen from around 1% of GDP in the 1930s to more than 6% of GDP in recent years. … At some point, this share has to stop rising and when it does, the implication is that this past source of growth will be unavailable.”

Fourth, “educational attainment is stagnating.” In recent years, Americans haven’t been getting more educated, as measured by average years of schooling. This means that the economy will not get the same boost from education as in the past when educational attainment was rising, which could lower economic growth by half a percentage point per year. What’s more, when rising research intensity levels out — the contribution of the rising investment share of intellectual property products — it could lower economic growth by another 0.7 percentage points per year.

Fifth, “population growth is slowing and may turn negative. If the entirety of the growth in living standards over the long run is due to population growth (“Income per person ← Ideas ← People”), then things look ominous given that in rich countries, Jones explains, “observed fertility rates are already consistent with a declining population rather than with a growing population. It is distinctly possible that the global population will level off and then start to decline over the next century. The implication for growth theory is that living standards could stagnate rather than continue to grow exponentially: If the number of people searching for ideas declines over time rather than rising, economic growth eventually comes to an end.”

➡ There are three headwinds that might offset those anti-growth headwinds: Asia, allocation of talent, and AI

First, “the rise of China and India.” The economic rise of China and India means the addition of lots of new people involved in idea generation. (Jones notes that in 2013–2016, Tsinghua University produced more of the 10 percent most highly cited papers in STEM than any other university in the world.) All this added brainpower means a bigger global research effort even as population growth rates are slowing.

Second, “improving the allocation of talent.” Jones points out that the US economy has benefited from the better allocation of talent across different groups of people over the past five decades. For example: Sandra Day O’Connor, the first woman Supreme Court Justice, faced discrimination in her early career despite her academic excellence. What’s more, research finds that being exposed to innovators as a kid raises the odds of a kid becoming an inventor. Jones: “Exposure in childhood is limited for girls, people of certain races, and people in low-income neighborhoods. So the opportunities to expand the talent for research are not only limited to China, India, and other developing countries. How many future Steve Jobs and Jennifer Doudnas are waiting to realize their potential?”

Third, “artificial intelligence.” Let me quote Jones at length since I think his observations here are super important:

The recent emergence of ChatGPT and other large language models indicates dramatic advances in artificial intelligence. Machines are increasingly able to substitute for humans in various tasks. We’ve argued that a lack of talented people to search for new ideas is an impediment to future growth. What if machines can replace people in this task as well? … [It] is at least possible for growth rates to rise if A.I. can partially or fully replace people in generating ideas. However, [there are also] various bottlenecks that can limit the extent of these effects. For example, automation has been going on since the Industrial Revolution. The steam engine, electricity, internal combustion engines, tractors, and semiconductors are all examples of amazing new technologies that helped automate various parts of the economy. And yet … none of these technologies accelerated growth during the past 150 years. The development of a new general purpose technology every few decades may be precisely what kept the 2% trend going for so long. Perhaps A.I. is just the latest amazing technology that will postpone a slowdown for several more decades and permit 2% growth to continue a bit longer. Sowhile it is conceptually possible for A.I. to raise growth rates, it is far from certain. Theory says it is possible while history gives reasons for caution.

Bottom line: Jones offers a realistic, if sobering, baseline that should set our current expectations about America’s future growth prospects. For example, it’s reasonable to view AI-machine learning and GenAI as a technological advance akin to the PC + internet combo rather than a sci-fi leap forward that will turn our current 2 percent trend in real GDP per capita into a 20 percent trend or something. That said, a big, frontier-leading economy that’s able to continue its long-term growth trend has surely accomplished something pretty impressive.

But I think we can do better. There’s reason to think that GenAI may be more important in productivity terms than the PC + internet combo. And public policy could do far more to help boost the productive capacity of the American economy. Even though the “investment rate in ideas” will flatten at some point, we could be investing a lot more in part of that IRI, specifically: basic science. Regular readers of this newsletter also know by now that we hardly have a regulatory structure in the US that is amenable to rapid technological deployment.

Faster, tech-driven growth is a national goal that will be difficult to achieve but also worth the effort — as I passionately argue through an economic, historical, and cultural analysis in 🚀 The Conservative Futurist: How to Create the Sci-Fi World We Were Promised.

Micro Reads

▶ Clean Growth - Costas Arkolakis and Conor Walsh, NBER | We find that the Inflation Reduction Action significantly hastens the adoption of renewable energy in the US, increasing renewable penetration by around 13% by 2030. It also has global spillovers, as the increased investment drives capital prices lower, increasing adoption in other countries around the world. The budgetary cost is substantial, coming in close to the budgeted cost of $160 billion. Much of the subsidy goes to inframarginal investment, which would have been installed in the absence of the IRA. Nonetheless, even without considering any benefits of carbon pollution reduction, we find that the IRA more than pays for itself. … Overall, the picture that emerges from our analysis is of a world undergoing rapid, beneficial change. Under all scenarios we consider, world power production is likely to shift fairly quickly to a grid dominated by renewables, bringing with it cheaper power and greater industrial output. Importantly, this conclusion holds when we conduct our analysis under a fixed transmission grid; we do not find the current grid structure in most countries to be inimical to renewable investment. As we discuss below, the modular nature of renewables and the speed of ongoing cost falls means that significant welfare gains are likely even without additional investment in grid infrastructure. In ongoing work, we consider the role of improving transmission linkages in further hastening clean growth.

▶ Are self-driving cars already safer than human drivers? - Timothty B. Lee, Ars Technica |

▶ COVID and cities, thus far - Gilles Duranton Jessie Handbury, VoxEU |

▶ US should use chip leadership to enforce AI standards, says Mustafa Suleyman - Richard Waters, FT |

▶ Meet Ernie, China’s answer to ChatGPT - The Economist |

▶ Germany begins dismantling wind farm for coal - Wester Van Gaal, EUobserver |

▶ Climate engineering: a quick fix or a risky distraction? - Aime Williams and Alice Hancock, FT |

▶ A Canadian study gave $7,500 to homeless people. Here’s how they spent it. - Sigal Samuel, Vox |

▶ The Battle Over Books3 Could Change AI Forever - Kate Knibbs, Wired |

▶ Ban or Embrace? Colleges Wrestle With A.I.-Generated Admissions Essays. - Natasha Singer, NYT |

▶ What Stephen King — and nearly everyone else — gets wrong about AI and the Luddites - Brian Merchant, LA Times Opinion |

▶ Why do we need infrastructure policy? - Brian Potter, Construction Physics |

Have interstellar meteor fragments really been found in the ocean? - Leah Crane, New Scientist |

>There are three headwinds

I assume this should be "tailwinds"?