🚀 Wall Street on SpaceX: 'Everything depends on Starship.' And they're right

The fully reusable mega-rocket could dramatically lower launch costs, opening the door to the New Space Age we’ve dreamed about since Project Apollo

My fellow pro-growth/progress/abundance Up Wingers:

With SpaceX joining the Nasdaq today, Wall Street banks are releasing their initial reports on Elon Musk’s rocket company. Goldman Sachs, a lead SpaceX IPO underwriter, initiated coverage with a “buy” rating and a 12-month price target of $205. JPMorgan, a secondary underwriter, gave the stock an “overweight” rating and a December 2027 price target of $225. They were hardly the most bullish.

I don’t directly own the stock, and I’m not super interested in the investment ratings and price targets. But I am definitely interested in how the banks see some of the key issues facing the company, particularly ones that overlap with an Up Wing vision of humanity becoming a true spacefaring civilization—and an AI/AGI-powered civilization via orbital AI data centers.

In short, what do the banks think about (a) the viability of Starship, and (b) assuming Starship will be a reliable, reusable, high-cadence vehicle, what does that mean for launch costs? Everything in these reports—and in an Up Wing vision of space—is downstream from a single number: dollars per kilogram to orbit. It’s the number that will determine the economic viability of humanity living and working in low-Earth orbit, colonizing the Moon and Mars (and beyond), and whether we can build space-based energy and AI infrastructure.

Given that these reports are from banks that underwrote the SpaceX IPO, you would expect them to be upbeat. But as I mentioned, they’re hardly the most optimistic. So maybe interpret the following analysis as the (reasonable) optimistic or bullish case.

One other thing: When discussing the potential of the space economy, I have frequently cited a thorough 2022 Citigroup report, “Space: Dawn of a New Age.” That analysis forecasts launch costs falling toward the same range now outlined in the GS and JPM reports. At those costs, Citi argued, space could evolve from a market dominated by government launch and satellite applications into a much broader (and exciting) economy: space-based solar, space logistics, commercial space stations, city-to-city transit, Moon and asteroid mining, tourism, and microgravity R&D. Citi ballparked those new applications and industries at roughly $100 billion in annual sales by 2040. It’s worth noting that these new Goldman and JPMorgan reports add an even larger possibility that Citi didn’t anticipate: orbital AI compute.

The Goldman Sachs view

Let’s start with the GS report. This may be the most important sentence in the report: “We expect Starship to become fully operational and prove out commercial viability in the coming quarters as the vehicle begins deploying internal (and in 2027, external) payloads into orbit.”

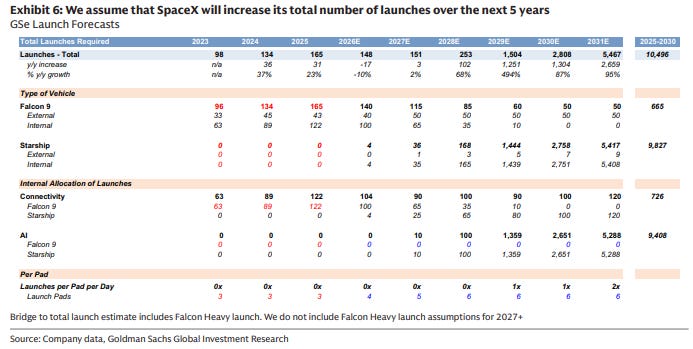

Yes, the report dutifully notes that failure is still a risk (same goes for an orbital compute buildout) that investors need to consider, but the GS model is assuming viability. That’s not to say it will be easy. The launch and production curve here is pretty wild. GS is expecting the “total number of Starship launches expected to reach ~2,750 in 2030” and that means SpaceX “will have to manufacture 600 Starships through 2029 to support launches.”

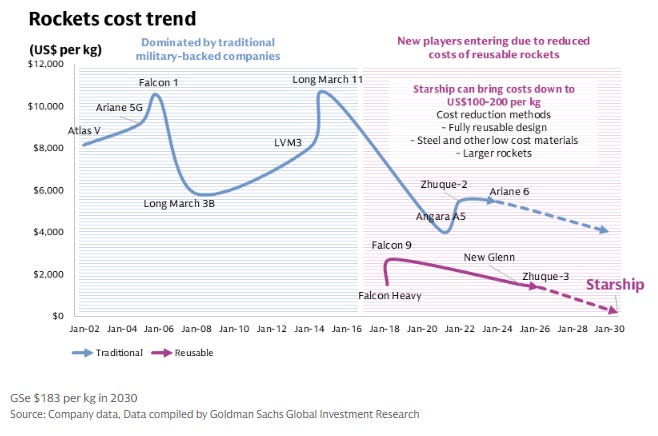

Starship reusability and launch cadence, if met, then lead us to the most important number in the GS report: "Relative to Falcon 9 (which has seen an 85%+ cost reduction relative to the overall industry), we expect that in 2030, Starship launch vehicles will reach $183 cost per kg (99.1% discount rate vs. SpaceX's long-term goal of 99%+)." Again, remember the aforementioned Citi report.

And what possibilities does that simply massive cost reduction create? For one thing, the math starts to work for a network of orbital data centers. (Sorry Down Wing, anti-AI NIMBYs, you are going to lose.) Goldman here models 47 AI satellites per Starship launch, with roughly 50,000 deployed in 2029 alone and 175,000 in orbit by the end of 2030. That gives a total of 26 gigawatts of orbital compute, or nearly three times the terrestrial compute Goldman expects SpaceX to have by then.

A caveat worth noting: The supposed cost advantage of building compute in orbit is an estimated $15–20 billion per gigawatt, versus $28–32 billion terrestrially. But that discount depends partly on the success of Terafab (the giant chipmaking project SpaceX plans with Tesla) to reduce reliance on Nvidia and other third-party suppliers.

As such, there needs to be successful execution on multiple ginormous industrial bets here, although GS concludes: “Longer-term, while the scaling effects of orbital compute is long duration in nature (and dependent in the medium term on the scaling of the Terafab project), the company seems uniquely (if not singularly positioned) against the current industry landscape to build a highly efficient AI infrastructure in space.”

While the orbital compute goal is AI-revolution friendly and eventually a revenue generator for the company, the main big-picture thing I was looking for was something like a legit business plan for leaving Earth.

Encouraging news, then: GS expects the Starlink satellite service to throw off so much cash in the coming years that it becomes “the capital source for both deeper space exploration (over a 10+ year horizon) as well as being an enabler of the capital needs for the AI business.”

And that leads to what the bank identifies as upside factors for the stock, many of which will be familiar to longtime SpaceX enthusiasts:

Better than expected execution on existing addressable market opportunities, along with growth into longer-term market opportunities which the company frames to include: a) point-to-point terrestrial travel, space tourism, in-orbit manufacturing, asteroid mining, manufacturing, energy and transportation solutions between the Moon and Mars.

The JPM view

No surprise: JPMorgan also sees Starship as the straw that stirs the drink; it drives the viability of the bullish SpaceX thesis. Nor is the bank subtle:

Everything Depends on Starship. We view Starship’s path to rapid and complete reusability as the critical enabler underpinning SpaceX’s many long-term growth drivers. Accordingly, any delays, technical setbacks, or regulatory hurdles that constrain the launch trajectory will impede planned growth across multiple business lines. Importantly, rapid reusability is expected to structurally lower launch costs 80%+ vs. legacy and unlock the ambitious launch cadence and delivery of mass required for Starlink’s next-gen capabilities, orbital compute, & the broader space economy. While SpaceX has an incredibly strong track record of innovation, with many key “firsts” across Space, Connectivity, and AI, Starship’s scale & complexity will require superior execution.

And what is the potential here?

SpaceX’s Mission Leads to Potentially the Largest Economic Frontier Ever. SpaceX’s ambitions are bigger than any company’s we’ve ever seen—to build the systems and tech to make life multi-planetary, to leverage the power of the Sun to help build out AI, and to ultimately build bases on the Moon and cities on other planets. Launch capabilities and achieving rapid reusability of Starship are at the core, and SpaceX is many years ahead in Space. Connectivity has driven recent financials as SpaceX produces & deploys thousands of satellites per year to operate the largest LEO constellation, which powers Starlink. The future should be driven by the AI segment as SpaceX is forecast to increase terrestrial compute capacity ~8x by 2028, and improve frontier model positioning and monetization through the combination of Grok and Cursor. SpaceX’s emerging cloud business also enables the company to capitalize on excess compute capacity at highly attractive economics, while retaining flexibility for internal projects. From 2029 on, we expect SpaceX to build out orbital compute, with rapid reusability of Starship ultimately driving tens to hundreds of GW of compute power, at a significantly cheaper cost than could be done on Earth. In our view, no other company is as well positioned to go after what SpaceX believes is a combined estimated TAM of more than $28T.

Like GS, JPM treats Starship viability as the core to its base-case assumption. Yet it’s also fully aware that the model depends on heroic execution on numerous fronts (again, I’m not offering investing advice here): full/rapid reuse, 100-ton payloads, massive production, more launch pads, regulatory approvals, fuel supply, and thousands of launches a year. Yeah, it’s a lot. Plenty of vectors for pessimists and bears.

Of course, there are lots of questions to be answered and here’s how the bank tackles the ones most central to the interests of this newsletter:

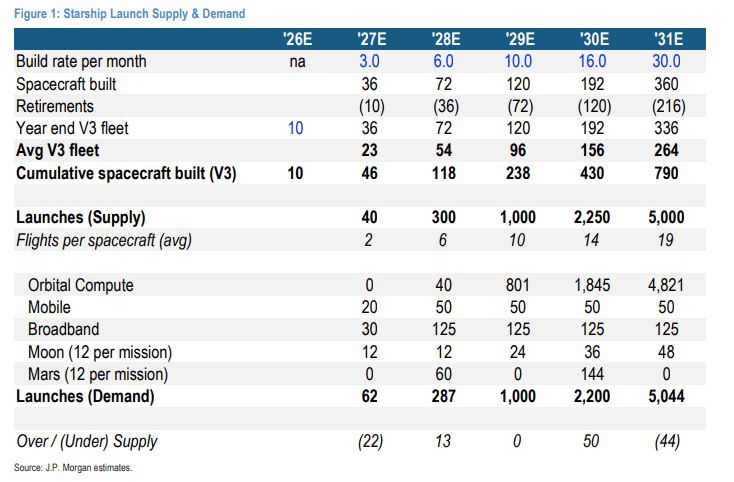

“Can SpaceX scale Starship launches to deliver massive orbital compute?” Sure, those 5,000 launches a year by the early 2030s are possible if a bunch of hard technical and regulatory problems I just mentioned, from second-stage reuse and turnaround to launch-pad approvals, are solved.

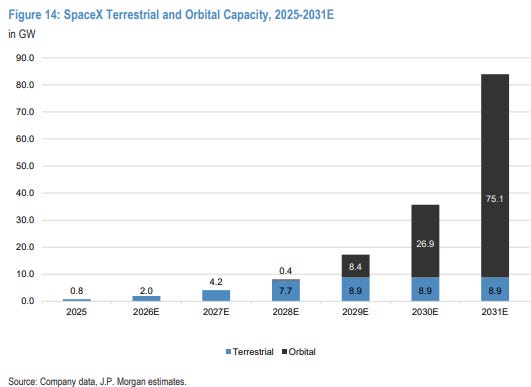

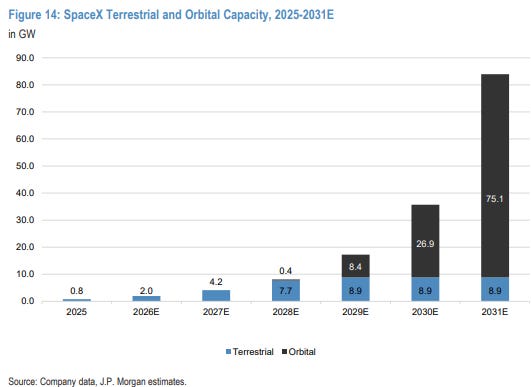

“Data centers in space…Why do they make sense and how does SpaceX plan to build them out?” If terrestrial AI buildouts keep running into power, land, permitting, and political constraints, yeah, shifting into orbit makes sense. “We expect SpaceX to begin launching its first operational AI satellites in 2028, with 0.4 GW of nameplate compute online by the end of the year. … By the end of 2031, we expect SpaceX to have completed over 7,000 launches and have 75.1 GW of compute capacity in orbit.”

“Dream the dream…what else could SpaceX do over time?” And I quote:

SpaceX has a proven track record of leveraging its differentiated capabilities across launch, engineering, & manufacturing to unlock and scale entirely new markets. While SpaceX believes it is already addressing the largest TAM in history across Space, Connectivity, & AI, the company’s ambitions extend far beyond that. … SpaceX’s stated foundational mission is to build the systems and technologies necessary to make life multiplanetary, with the long-term goal of establishing a self-sufficient city on Mars. The company estimates that such a city would require ~1M people and millions of tonnes of cargo, delivered by several thousand Starships across launch windows that open only once every ~26 months, when Earth & Mars are favorably aligned. SpaceX has indicated that uncrewed Starship cargo flights to the Martian surface for research & exploratory missions could begin as early as 2028, while NASA is working to send astronauts to Mars as early as the 2030s. While establishing a city on Mars certainly ranks among the most ambitious goals we have seen, and one that likely remains distant, if achievable at all, we believe SpaceX will leverage the Moon as a critical proving ground for the habitats, resource utilization, & Starship systems that any eventual path to Mars would depend on.

Bottom line: If any of this if possible, there is no company better positioned than SpaceX to make it happen.

On sale everywhere The Conservative Futurist: How To Create the Sci-Fi World We Were Promised

I am not an engineer. But these starships keep blowing up. Getting them to work and become reusable is unclear and if not the stock will crater. The Mars scenario is sci-fi.