Tyler Cowen on the end of the Great Stagnation

Plus: bad news for Elon Musk's hyperloops; why most of the value created by Jeff Bezos doesn't go to Jeff Bezos; looking for a pro-growth tax code, and much more ...

“As long as the roots are not severed, all is well. And all will be well in the garden. … In the garden, growth has it seasons. First comes spring and summer, but then we have fall and winter. And then we get spring and summer again.” - Chance the Gardener, from the 1979 film Being There.

In this Issue:

⏩ Is the Great Stagnation Over? A Q&A with Tyler Cowen (1220 words)

🚄 How environmental rules are killing Elon Musk’s hyperloop dream (389 words)

📦 Most of the value created by Jeff Bezos and Amazon doesn’t go to him (375 words)

💵 Does America have a pro-growth tax code? (388 words)

⏩ Is the Great Stagnation Over? Here’s what Tyler Cowen thinks

Back in 2011, economist Tyler Cowen wrote The Great Stagnation, addressing the American economy’s productivity slowdown since 2005 and, really, since the early 1970s. A decade later, there are intriguing hints that we are entering, dare I say, a Great Acceleration.

![The Great Stagnation: How America Ate All The Low-Hanging Fruit of Modern History, Got Sick, and Will (Eventually) Feel Better: A Penguin eSpecial from Dutton by [Tyler Cowen]](https://substackcdn.com/image/fetch/$s_!FK7u!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F19f930cd-7e59-442c-9889-c6b15f2a66d8_387x500.jpeg "The Great Stagnation: How America Ate All The Low-Hanging Fruit of Modern History, Got Sick, and Will (Eventually) Feel Better: A Penguin eSpecial from Dutton by [Tyler Cowen]")

Sure, this year and next might be pretty growthy thanks to the tsunami of federal spending and vaccine-driven economic reopening. But amid this stimulative surge, might there be something deeper and more durable happening to boost the economy’s productive capacity? Last year was a pretty impressive year for technological progress, from rapid vaccine innovation to a new age of human spaceflight for America. And the pandemic itself might play a role, pushing companies to adopt a host of new technologies, along with “the accelerated move online, more judicious business travel, and work-from-anywhere,” as this newsletter quoted Moody’s Analytics economist Mark Zandi last week.

So is the Great Stagnation over? Here’s how Cowen addressed that question in a recent AEI panel that I moderated (edited for clarity):

Pethokoukis: Tyler, you wrote a book called “The Great Stagnation,” and it’s been 10 years since you published that book. What was your argument at the time about the great stagnation and why we were stagnating?

Cowen: At the time, I suggested that our previous technologies had, in some regards, run their course. If you take powerful machines and fossil fuels and put them together as a kind of general-purpose technology, we did everything we could with that. We invented cars, and then almost everyone had a car. And then cars got better, but they just didn’t get all that much better.

I think the odds are we are, today, on the cusp of another revolution based on new general-purpose technologies, which I would define as some mix of internet, computers, and computational power. So in 2011, when I published the book, I thought the great stagnation would end within the next 20 years, and odds are what we’re seeing today is the great stagnation ending.

We’ve come up with great new ideas, took a little while to figure out how to use them and how to spread throughout the economy, and eventually they made big differences. Are we assuming that these new technologies are like the ones in the past and they'll have that eventual impact?

I think the new innovations will be special in at least one significant way: A lot of them will not contribute that much to per capita GDP. So, if you take the mRNA vaccines, they’re influencing what would normally be called the “cyclical component.” If you think of older people as more likely to die from COVID-19 . . . by saving lives — I’m not suggesting per capita GDP will go down — but the impact on human welfare will be much greater than what would appear to be the long-term secular trend in GDP. Also, two of the big advances that might happen are a vaccine against HIV/AIDS and an effective vaccine against malaria. Those would be incredible advances for humanity, but I don’t know how much they would show up in US per capita GDP or productivity — possibly not really much at all.

The other new wave of innovations, which you could call green energy — again, you could be very optimistic about those, but the main thing they’re doing is helping us avoid a catastrophe. So they’re boosting GDP relative to a quite awful counterfactual of just continuing to burn coal and other fossil fuels. But I’m not sure we’ll feel we have higher standards of living relative to what we were used to simply because there’s a solar panel on your home. It might in some ways make your energy supply better, but again, it will be hidden by the counterfactual. So, it will be a very strange kind of technology boom when I look at the two main areas where I see a lot of progress.

If we go through a period where none of this stuff is really showing up in data and maybe it’s not obvious that people’s living standards are rising, do we risk having less societal tolerance for the kinds of disruptions that economic growth and progress naturally make?

Here’s one of my fears: The biomedical innovation progress is so fast but the rest of the economy stays relatively static, so we become older as a society more quickly than we had been expecting. You could have a lot more status quo bias — just more entrenchment, 10 years more of a problem — and we could, in a funny way, innovate ourselves into a tighter complacency and a tighter stagnation.

I’m not rooting against increases in life expectancy. Ceteris paribus, I would take them, obviously. But that said, you want to be careful about the order in which progress comes, and I’m not sure if we’re going to get it in an optimal order.

What is your confidence level that all of these technologies, such as AI, won’t create widespread unemployment — that they will enhance what we do and create new things for us to do, and they’re not just going to end up being job–replacing technologies?

I’m not so worried about job loss. I’m more worried that the internet makes people weirder. Now, that makes them more creative, it creates small groups, it’s very fruitful, it can be fun and exciting. But viewed anecdotally, it seems reasonably obvious to me the internet is making us weirder on the whole in a QAnon sort of way, and that intersects with a fairly large government. And I don’t think we have any good models for how that process works — either on the psychological side or the political science governance side. So I’m broadly worried about that: Without having a clear prediction, it just seems to me the political equilibria we used to have are just not coming back.

An acceleration may not be obvious in all the economic statistics, but shouldn’t it be obvious in some statistics? If we’re going to see an acceleration in technological progress, wouldn’t it show up somewhere?

Cowen: Public health statistics. But I think there’s one innovation, in particular, we haven’t discussed yet, and it could be the most important one: innovations to make raising children easier. Raising children is one of the great joys of life, but it’s also one of the great burdens. And I see really quite a few wealthy countries depopulating. If we don’t have innovations to make raising children easier, more fun, or less costly, we’re in big trouble. So let’s not only talk about per capita GDP; let’s talk about the number of capitas. And that’s possibly a crisis — I would say already a crisis for Italy, and maybe Japan and South Korea.

If we had this seminar 10 years from now, and it’s titled “Why the Great Stagnation continued,” and there was no Great Acceleration, do you think it’s more likely to be because the technologies that we’ve mentioned really didn’t turn out to be that transformational? Or do you think it’s more likely that we implemented policies that are actually harmful to economic growth and productivity growth?

Cowen: I have a different nomination: I would say it’s that we had some emergencies, we responded pretty excellently, and then we sunk back into our sloth.

🚄 How environmental rules are killing Elon Musk’s hyperloop dream

NASA just picked Elon Musk’s SpaceX to land the next Americans on the Moon. But as the world’s second-richest person (I’ll get to the world’s richest person in a bit) is finding, it’s harder to get government approval to do things below the Earth than above it.

Back in 2017, Musk said he wanted to connect Washington and Baltimore with a hyperloop, a high-speed, underground train. It was to be the first segment of a bigger project linking the nation’s political capital with its financial capital, New York City via a half-hour train ride. A year later, Musk announced the Dugout Loop that would whisk baseball fans from Los Angeles neighborhoods to Dodger stadium at speeds up to 150 miles per hour.

Both projects now look moribund. As Bloomberg reports, “Both projects are currently mired in a regulatory no man’s land of environmental review and have not broken ground. Now, Boring Co. has removed all mention of either of them from its website—a suggestion that Musk is backing away from the projects.”

One can want (a) clear air and water, (b) to avoid devastating climate change while also (c) thinking that environmental regulation has made it unnecessarily hard to build things in this country. And whether or not one thinks the trade-off is worth it, this trade-off exists. In the 2020 paper, “Infrastructure Costs” persuasively, I think, connects 1970s environmental regulation — particularly federal statutes like the National Environmental Protection Act that boosted “citizen voice” litigation — for the more than three-fold increase in real spending per mile on Interstate construction from the 1960s to the 1980s.

Moreover, an analysis last year from Brookings Institution economist Clifford Winston finds average time to complete a NEPA environmental review has “grown sharply over time and that the permitting process for major projects may take as long as ten years.” Today the average Environmental Impact Statement runs more than 600 pages and takes 4.5 years to complete. And no ground can be broken, a recent Niskanen study notes, “until the EIS has made it through the legal gauntlet.”

Hyperloops may be a dumb idea — or an impossible idea. But if you want a clean energy revolution, then you want NEPA reform. When such reforms were proposed by the Trump administration last year, many geothermal, solar, and wind advocates were delighted. Too bad, the Biden administration might reverse them.

🚚 Most of the value created by Jeff Bezos and Amazon doesn’t go to Jeff Bezos

Amazon founder Jeff Bezos is worth nearly $200 billion. And at the moment that makes him the richest person on Earth. So he’s clearly created a lot of value for himself since he wrote his first letter to Amazon shareholders back in 1997. In his latest letter — also his last since he’s stepping down as CEO — Bezos gives a more comprehensive view of who’s benefited from the growth of a company now with a market capitalization of nearly $2 trillion. One group, of course, are shareholders not named Jeff Bezos, who own 7/8th of the shares and include pension funds, universities, and 401(k)s.

But there’s more to the story here than what Bezos calls “shareowners.” A lot more. Bezos looks at it this way, using the example of last year’s corporate performance: Firstly, Amazon created $21 billion in value for shareholders in 2020, or the company’s net income. If Bezos owned the whole kit and caboodle, that’s how much he would have earned last year. Secondly, there’s the $91 billion (payroll plus benefits and payroll taxes) of compensation for Amazon workers. Thirdly, third-party sellers earned somewhere between $25 billion (Bezos’ “conservative” choice) and $39 billion in profits. Fourthly, Bezos assigns $126 billion (75 hours saved a year shopping online x $10 an hour - the cost of a Prime membership) to Amazon’s "consumer customers,” including the 200 million Prime members. Fifthly and finally, Bezos pegs “AWS customer” value creation at $38 billion, based purely on cost savings and excluding the benefit from faster software development.

This back-of-the-envelope calculation (and there’s greater detail in the letter) works to total value created of $301 billion, with just 7 percent of that going to shareholders. And since Bezos owns less than 10 percent of the shares, the value going to Amazon founder last year works out to about $2 billion, or less than 1 percent of total value created.

The estimate reminds me of the great paper from Nobel laureate economist William Nordhaus, “Schumpeterian Profits in the American Economy: Theory and Measurement.” Nordhaus tries to calculate who gains from the value generated by innovation. His findings: “We conclude that only a minuscule fraction of the social returns from technological advances over the 1948-2001 period was captured by producers, indicating that most of the benefits of technological change are passed on to consumers rather than captured by producers” And by “most,” he means almost all of the benefit with innovators “able to capture about 2.2 percent of the total social surplus from innovation.”

Makes a rough sort of sense when you think about it. Consider what Jeff Bezos is worth — a lot — versus the value generated by his nearly trillion-dollar company — a whole lot more — and benefits all of us accrue. Not sure the “billionaires are policy mistakes” folks really get this.

💵 Does America have a pro-growth tax code?

The American economy won’t crash if President Biden is successful in raising the corporate income tax rate to 28 percent from 21 percent. That said, a hike to 25 percent seems more politically likely. JPMorgan is telling clients it expects a “relatively modest effect on capital expenditures if the corporate tax rate were to rise by a few percentage points.”

A key reason for this benign view is that there’s more to the corporate tax code — and how it affects business investment decisions — than the tax rate. The current code also temporarily allows full and immediate expensing of short-lived capital investments. (Should be made permanent.) Yet even before the 2017 Trump tax cuts, the tax code was pretty pro-investment. JPM: “The US corporate tax code was quite close to allowing the immediate deductibility of capital expenditures from income, due to “bonus depreciation” provisions and historically low interest rates.”

Smart tax reform, unlike the Biden plan, should make it more attractive for companies to earn after-tax income generated by new investment. More investment makes workers more productive and, over time, raises wages. Taxes matter for economic growth and living standards. That is something policymakers must remember. There’s no money tree. America’s fiscal trajectory means taxes will need to go up — and not just on companies and rich people. Washington will need to tax in ways that raise needed revenue and are economically efficient. That probably means eschewing new wealth taxes, although lots of folks on the left are talking about them. As AEI economist Kyle Pomerleau told me last year:

I think the concern is that you take the wealth tax, you stack it on top of the higher corporate tax, and you stack it on top of the changes to capital gains taxes. That all means that the United States overall becomes less favorable to entrepreneurship and risk-taking. The total returns to risk — taking the risk and becoming an entrepreneur — go down. So you get less of that activity. The US is somewhat of a low-tax country. That’s where we can have some advantage in entrepreneurship and risk-taking.

So we’re probably talking about a national consumption tax, possibly paired with a carbon tax that replaces the corporate tax in part or whole. That’s not where the debate in Washington is right now. But it eventually has to be.

Redesigning AI - Boston Review | This is a long essay by MIT economist Daron Acemoglu, who’s been researching the impact of AI on the economy, especially labor markets. A taste: “Our current trajectory automates work to an excessive degree while refusing to invest in human productivity; further advances will displace workers and fail to create new opportunities (and, in the process, miss out on AI’s full potential to enhance productivity).”

With Economy Poised for Best Growth Since 1983, Inflation Lurks - Wall Street Journal | Economists surveyed boosted their average forecast for 2021 economic growth to 6.4 percent (measured as the change in inflation-adjusted gross domestic product in the fourth quarter from a year earlier.) That’s a big jump from last December when they expected 3.7 percent growth, “reflecting the reversal of pandemic-induced shutdowns as well as the Fed’s low interest rates.”

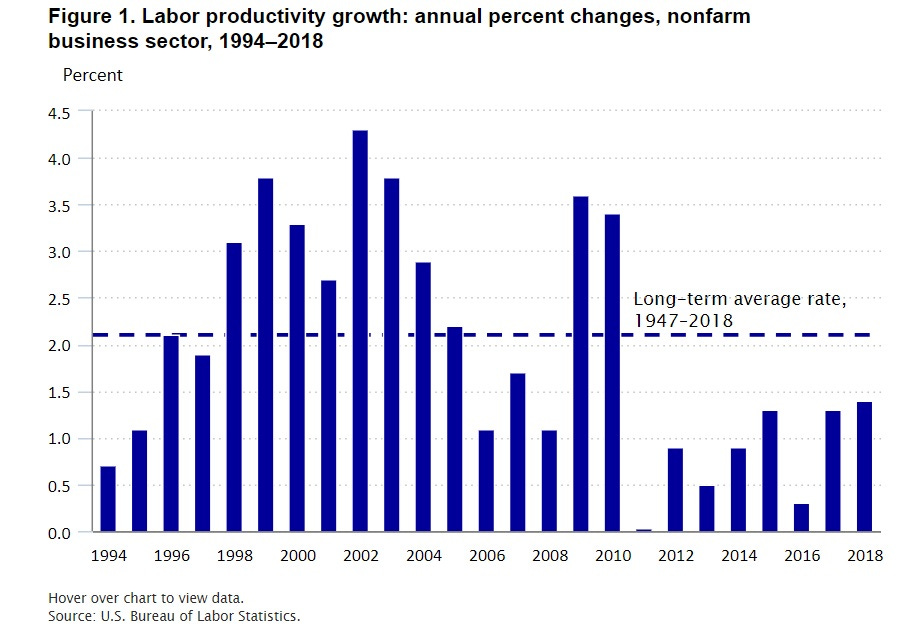

The U.S. productivity slowdown: an economy-wide and industry-level analysis - Bureau of Labor Statistics | A fantastic explainer of this long-term problem. I think the lede sums things up nicely: “The figure—$10.9 trillion—represents the cumulative loss in output in the U.S. nonfarm business sector due to the labor productivity slowdown since 2005, also corresponding to a loss of $95,000 in output per worker.”

Flying cars finally prepare for take-off - Financial Times | Columnist John Thornhill writes that investors “are pouring money into urban air mobility (UAM) companies in the expectation that they will be ferrying passengers around cities by the middle of this decade.” Among the key enabling tech advances: battery tech, autonomous driving systems, 5G networks, and low earth orbit satellite constellations.

Biden touts trains as fast as planes, supersonic jets in infrastructure push - NY Post | The headline doesn’t do justice to the vision being presented by Biden, one where supertrains crisscross the country as fast as airliners, and hypersonic planes — or maybe suborbital rockets — can get you to anywhere on the planet in about an hour, or about 21,000 miles per hour. It’s a throwback to the 1960s techno-optimism of Isaac Asimov and Arthur C. Clarke.

Biden’s science budget for 2022 pleases US research community - Chemistry World | We’ll see what makes it into law, but a clear change of pace from the past previous four years. “This is of course very different to what we saw from the previous administration,” says Matt Hourihan, who heads the AAAS’s R&D budget and policy programme. “The Trump White House proposed the most difficult budgets for science and technology of any administration since World War II.”

Geoengineering: What could possibly go wrong? - Bulletin of the Atomic Scientists | Under a White Sky, the title of Journalist Elizabeth Kolbert’s new book, refers to a possible unpleasant result of geoengineering the atmosphere to better reflect sunlight. Yet this Q&A seems to suggest Kolbert is a reluctant advocate: “My impulse as an old-school environmentalist is to say ‘Well, let’s just leave things alone.’ But the sad fact is that we’ve intervened so much at this point that even not intervening is itself … an intervention.”

Research and Development in the Pharmaceutical Industry - Congressional Budget Office | Lots of fascinating info here, including this: “In 2019, the pharmaceutical industry spent $83 billion dollars on R&D. Adjusted for inflation, that amount is about 10 times what the industry spent per year in the 1980s. Between 2010 and 2019, the number of new drugs approved for sale increased by 60 percent compared with the previous decade, with a peak of 59 new drugs approved in 2018.” These numbers also seem to support the “good ideas are getting harder to find” thesis.