🌐 Trump boom vs. tariff doom

Markets are sending a message. The White House should listen

I’m going to pass on any “new golden age” snark here. I would love for the next four years to be boomy ones — the full 1990s or better — whatever the metallic descriptor. And I think some of President Trump’s early moves on AI and energy infrastructure deregulation are pro-growth harbingers with hopefully more to come. Necessary moves? For sure. Sufficient? Apparently not.

That’s the message being sent by the Investor Class. Stocks plummeted today as recession (or maybe even stagflation) anxieties intensified, with the Dow Jones industrials shedding nearly 900 points. The sell-off gathered momentum after President Trump acknowledged a potential "transition period” (in stark contrast to his commerce secretary's categorical denial of recession prospects).

Investors appear disconcerted by what they perceive as the administration's hand-wavy, nonchalant attitude toward economic pain caused by his tariff-driven trade policy. As one investment analyst told the Wall Street Journal: “This is the first time we've had an administration pretty much say with a straight face [that] the objectives are going to cause pain.”

So long, animal spirits

Wall Street’s concerns were captured in a morning Goldman Sachs research note. The bank’s economics team has been one of the most bullish on Wall Street, and in their note they reiterated that Trump’s tax cut and deregulatory agenda would likely be supportive of growth. You love to hear it.

But his trade agenda? Not so much. What we’re seeing now is the erratic unfolding of a trade scenario that is worse than what the bank and the rest of Wall Street expected heading into 2025. At the time, GS warned that tariffs with the impact of what Trump is now doing “might lead to a considerably worse market sell-off” than during Trump’s first term.

GS (bold by me):

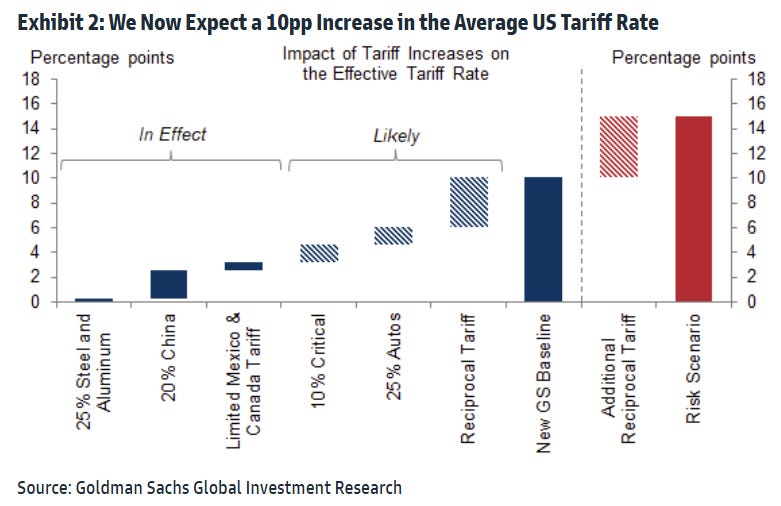

We have downgraded our 2025 US GDP growth forecast from 2.4% at the start of the year to 1.7% now (both on a Q4/Q4 basis). This is our first below-consensus forecast in 2½ years. … [The] reason for the downgrade is that our trade policy assumptions have become considerably more adverse and the administration is managing expectations towards tariff-induced near-term economic weakness. We now see the average US tariff rate rising by 10pp this year, twice our previous forecast and about five times the increase seen in the first Trump administration. While President Trump ended up softening the 25% tariff on Canada and Mexico soon after implementation, we expect the next few months to bring a critical goods tariff, a global auto tariff, and a “reciprocal” tariff. The reciprocal tariff matters most, not because other countries impose much higher tariffs on the US than vice versa—with a few exceptions such as India they don’t—but because the administration views e.g. Europe’s VAT of 20% as equivalent to a tariff (even though it is imposed equally on imported and domestically produced goods). If applied mechanically, a VAT-inclusive reciprocal tariff alone could raise the average US tariff rate by 10pp or more. Carveouts will probably lower this number, but if they are less widespread than we expect, the average tariff rate could rise as much as 15pp.

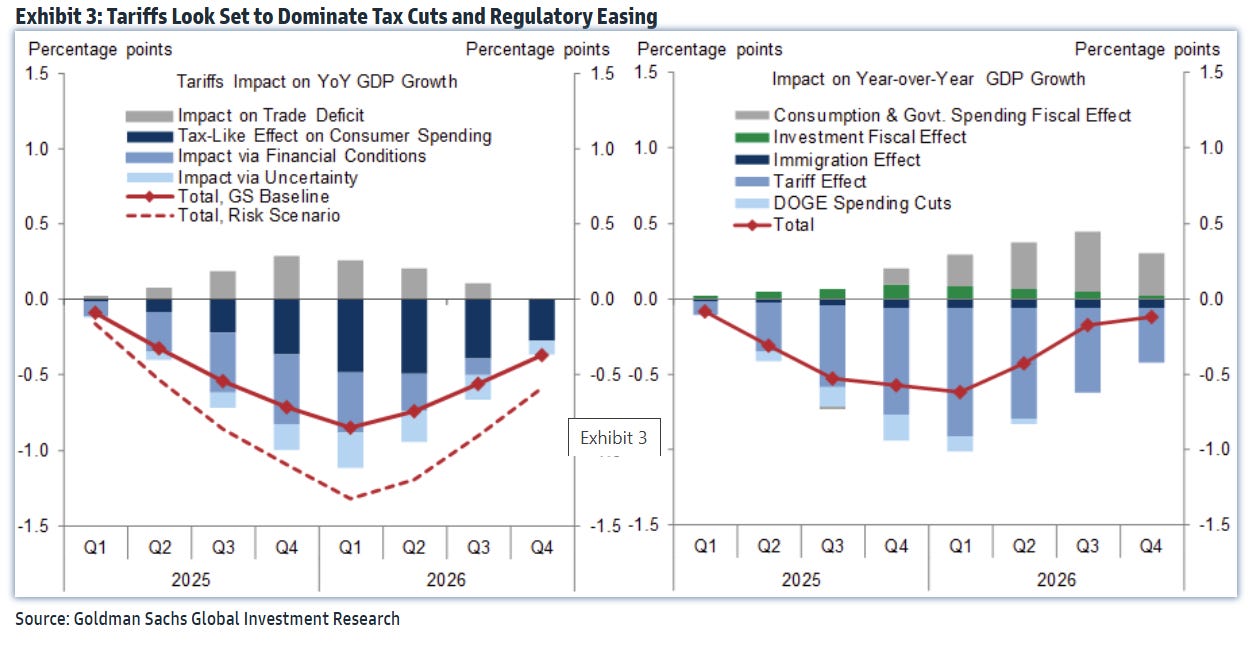

The GS team goes on to explain that it sees the Trump tariffs hampering economic expansion through three primary channels: reducing real incomes via higher consumer prices, tightening financial conditions, and delaying business investment due to policy uncertainty. The net effect: Tariffs are expected to subtract 0.8 percentage points from GDP growth over the next year, with tax cuts and deregulation offsetting only 0.1-0.2 percentage points of this drag.

Problematic populist economics

In other words, the pluses of traditional GOP-type economics are more than offset by the negatives of the new populist GOP economics. At least for now, by the way, investors don’t seem to be assuming a massive economic acceleration from AI or even AGI to make the US economy so bulletproof that even terrible policy — which a tariff-driven economic agenda is — can’t screw up things. Nor should policymakers be tempted by any such assumption.

Open trade, especially with other liberal democracies, is an important element of my Up Wing agenda. The nexus between free trade and economic growth has been central to economic theory since Adam Smith. To repeat: Nations benefit by specializing in goods and services where they possess comparative advantage. Access to larger markets enables firms to achieve economies of scale, spreading fixed costs across expanded production. Trade accelerates technological diffusion globally, whilst import competition erodes domestic monopolies and spurs innovation.

Let’s hope the market’s nasty reversal prompts an equally sharp reversal in Trump trade policy.

On sale everywhere The Conservative Futurist: How To Create the Sci-Fi World We Were Promised

Micro Reads

▶ Economics

Without Federal Spending, What’s Left of US GDP Growth? - Bberg Opinion

Digital Assets and Blockchain Through an Economics Lens - Richmond Fed

The folly of America’s R&D cuts - FT Opinion

▶ Business

Trump needs to find a solution for Intel - FT Opinion

Shareholder Capitalism Is Back - Bberg Opinion

▶ Policy/Politics

There Is a Liberal Answer to Elon Musk - NYT Opinion

Trump is making Europe great again - FT Opinion

▶ AI/Digital

What AI can currently do is not the story - Epoch AI

▶ Biotech/Health

Why nothing matters - Aeon