💥 The shocking return of zombie economics in 2021

Also: the demise of BBB; innovation in science research; neurotechology; and more ...

“Without continual growth and progress, such words as improvement, achievement, and success have no meaning.” - Benjamin Franklin.

🎄 Note to my wonderful Faster, Please! subscribers: This newsletter will be modified, both in format and publishing schedule, between now and year’s end. Have a wonderful holiday season! And please tell your family, friends, and colleagues — even randos on the street — to check out Faster, Please and subscribe!

Long Read

💥 The shocking return of zombie economics in 2021

Washington may not have an interest in economic orthodoxy, but Econ 101 sure has an interest in Washington and its choices. That reality should inform the 2022 decisions of policymakers, as well as the conversation on EconTwitter. Indeed, social media told me over and over that this was supposed to be the year that the “zombie economics” of dead economists (as well as the very-much-alive Larry Summers) lost their hold on the practical men and women of the White House and Congress — all, of course, to the benefit of the American businesses, households, and workers.

For example: The long-time consensus on unemployment benefits is that the duration of jobless spells increases with benefit generosity. But some early pandemic-era data challenging this consensus led very quickly to a new consensus — at least among many journalists and left-of-center policy pundits — that more generous benefits had tiny or even negligible effects on the US labor market.

But now there’s new evidence for the old consensus, courtesy of the new NBER working paper “Did Pandemic Unemployment Benefits Reduce Employment? Evidence from Early State-Level Expirations in June 2021” by Harry J. Holzer (Georgetown University), R. Glenn Hubbard (Columbia University), and Michael R. Strain (American Enterprise Institute).

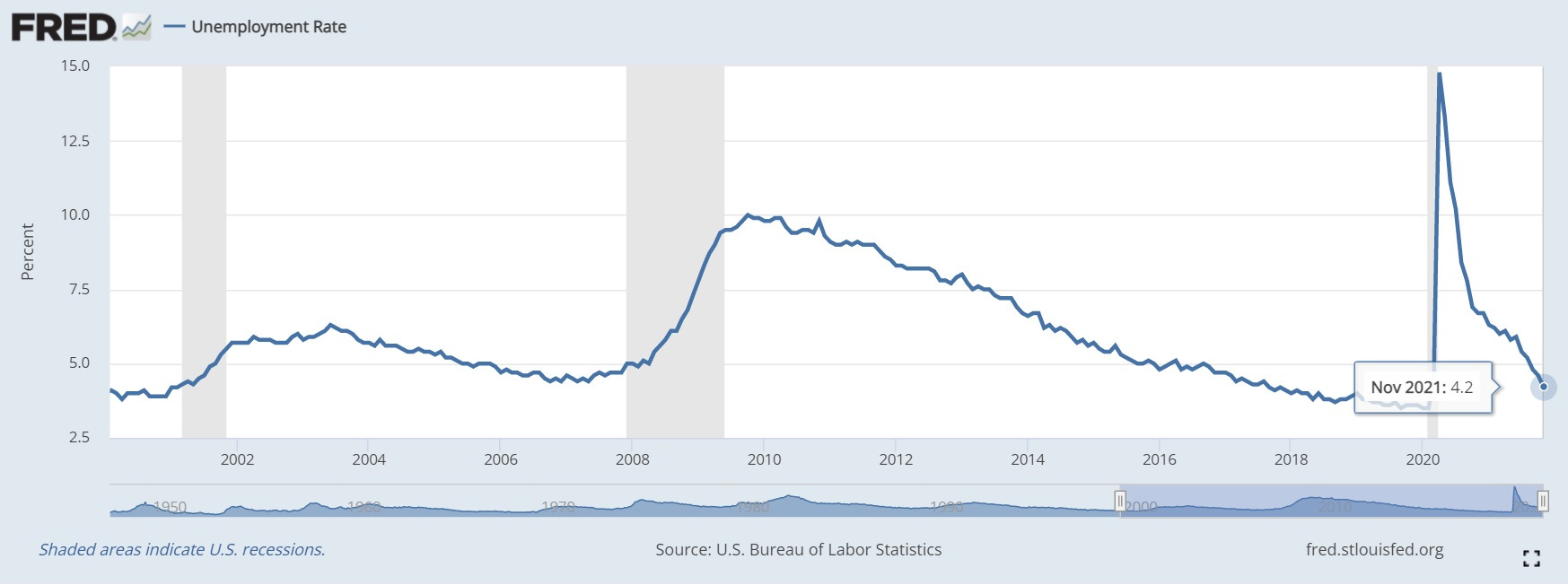

Recall that the American Rescue Plan, enacted back in March, extended programs that expanded jobless benefits to workers who are typically ineligible for state unemployment insurance programs — such as freelancers and independent contractors — and added a $300 weekly bonus to standard state UI benefits. But 26 states chose to opt out of at least one of those two federal programs before the September 6, 2020, expiration date, with 18 ending participation in both programs in June 2021. That left 24 states and the District of Columbia participating until the federal programs expired.

Using Census Bureau data, Holzer, Hubbard, and Strain create a counterfactual: What if those 24 states had also opted out of both programs in June? From there, the economists examine what the unemployment rate and employment-population ratio (the portion of people employed against the total working-age population) might have been in those two dozen states under their counterfactual. From the paper (bold by me):

We use these estimates in a simple counterfactual exercise to examine what the unemployment rate and employment-population ratio might have been if the 24 states and the District of Columbia that participated in FPUC and PUA through September had instead opted out in June. In those states, workers ages 25-54 would have had an unemployment rate 0.8 percentage point lower in July and 0.7 percentage point lower in August. Employment rates would have been 0.7 percentage point and 0.6 percentage point higher in July and August, respectively. The differences between the actual and the counterfactual unemployment rates are larger for workers ages 16-64, while counterfactual employment rates are roughly the same.

We extend this exercise to determine what the national unemployment rate and employment-population ratios would have been if all states opted out of pandemic-era UI programs in June. We estimate that the national unemployment rate in July would have been around 0.3 percentage point lower and the aggregate employment rate in July would have been 0.2 percentage point higher. In August, the unemployment rate would have been around 0.3 percentage point lower and the employment rate about 0.1 percentage point higher. The differences between the actual and counterfactual unemployment and employment rates using estimates from workers ages 16-64 are larger.. . . Consider that it took five months for the unemployment rate to increase 0.4 percentage point after the Great Recession begin in 2007 following the onset of the global financial crisis. While the economy was in recession in 2001, the unemployment rate increased by 1.2 percentage points in total.

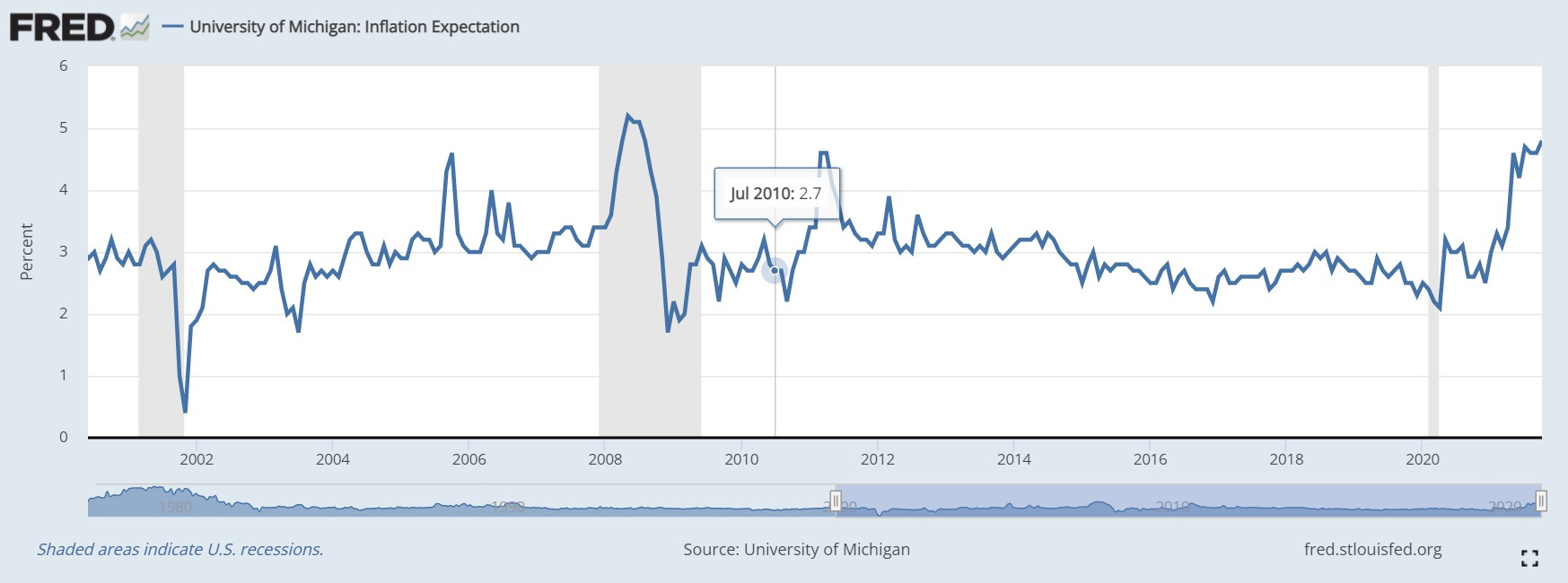

At least when it comes to the impact of jobless benefits on joblessness and employment, the economic fundamentals may well still apply. And you can add these findings to the Econ 101 lesson that we are re-learning about inflation: Whatever the reasons behind spiking prices — such as, perhaps, a tsunami of government dough flooding into a supply-constrained US and global economy — they can quickly change consumer perception and expectations. According to the University of Michigan’s Consumer Sentiment index out last month, inflation fears are growing. Consumers expect prices to rise by nearly 5 percent over the next year, the highest level since the summer of 2008. The risk here is that inflationary psychology becomes entrenched, requiring a nasty recession to reset expectations and prevent a price spiral. Inflation is not forever and always quiescent, just a thing of the 1970s and never again.

Serious policymaking should always be grounded in a realistic appraisal of both possibilities and constraints. If you don’t like, say, the reality that the US economy can still fall victim to inflation pressures, then spend prudently in the short run while working hard on policy to expand its long-term productive capacity. (Something this newsletter spends considerable space exploring.) Likewise, ignoring incentives and their impact on human behavior will lead to suboptimal policy choices. Let’s do better in 2022.

Micro Reads

📉 Build Back Better Unlikely to Pass; Lowering GDP Forecast - Goldman Sachs | Wall Street has been expecting BBB to pass, even as the topline number has come down. But Senator Joe Manchin had other ideas: GS:

A failure to pass BBB has negative growth implications. We had already expected a negative fiscal impulse for 2022 as a result of the fading support from COVID-relief legislation enacted in 2020 and 2021, and without BBB enactment, this fiscal impulse will become somewhat more negative than we had expected. Specifically, the expiration of the child tax credit and the lack of the other new spending we had been expecting will reduce the fiscal impulse to growth by around 1pp in Q1, 0.5pp in Q2 and 0.25pp in Q3. With this change, our GDP forecast for 2022 now stands at 2% in Q1 (vs. 3% prior), 3% in Q2 (vs. 3.5% prior) and 2.75% in Q3 (vs. 3% prior).

🧪 Can a new approach to funding scientific research unlock innovation? - Kelsey Piper, Vox | We should want science researchers to spend max time, you know, researching science! We don’t want them spending half their time writing grant proposals. Nor should we want them to be overly cautious in what they study in order to raise money. Thus pro-progress types should welcome the new biomedical research institute, called the Arc Institute, a nonprofit collaboration between Stanford, UC Berkeley, and UC San Francisco. ARC will be funded by some big names techies, including Patrick Collison, CEO of Stripe, and one of the Institute’s funders. “Researchers get eight-year grants to do whatever they want, instead of three-year grants tied to a specific project.”

😔 Alone and lonely: The economic cost of solitude - Chiara Burlina, Andrés Rodríguez-Pose, VoxEU | A super interesting conclusion: “Greater shares of people living alone drive economic growth, whereas an increase in loneliness has damaging economic consequences.”

🏙 An interview with Edward Glaeser: On urbanization, the future of small towns, and "Yes In My Back Yard" - David A. Price, Richmond Fed | The Harvard economist offers intriguing analysis on a number of issues facing pandemic-era America, including the future of small towns, the wisdom of place-based economic policies, and how to make sure housing reform doesn’t totally ignore local interests.

🧠 Neurotechnology must not treat humans like mice - John Thornhill, Financial Times | Neurotechnologies allow for the interface of the human brain and computers, with medical applications including the creation of prosthetics controlled by the mind and restoration of hearing to the deaf. But researchers have also been able to use neurotechnology to “generate false memories” in order to “manipulate” the actions of mice, spawning ethical questions about the use of this technology. In response, Chile has become the first country to enumerate neuro-rights into its constitution. But some experts warn that enshrining these rights into law may entrench narrow definitions of personal freedoms while clearing neurotech developers of their responsibility to prevent misuse of this technology.

⚡ Energy investment needs to increase — so bills and taxes must rise - The Economist | From the piece:

Meanwhile a chaos of mixed signals — stigma, virtue-signalling, subsidies, legal cases and regulations — means that investment in the energy industry is running at less than half the $5trn annual rate needed to get to net zero by mid-century. . . . In response, governments will expand the use of carbon prices, which act as an economy-wide ratchet on emissions. They will experiment with setting prices far into the future to give investors more predictability over the 20- to 30-year life-cycle of energy projects. America will remain an outlier, with no federal carbon price, but more Republicans will realise that pricing is the capitalist way to reform the energy business.

☁ Will cloud computing create a New Roaring ’20s? My long-read Q&A with Mark Mills - James Pethokoukis, AEI | Marks Mills is a Senior Fellow at the Manhattan Institute and the author of The Cloud Revolution: How the Convergence of New Technologies Will Unleash the Next Economic Boom and A Roaring 2020s. In a recent podcast chat, Mills described how the buildup of warehouse-scale data centers for cloud computing is a consequential investment in infrastructure that could be the key to great economic growth in this decade. “By all measures — dollars, physical equipment, square feet of buildings — [the cloud is] the biggest infrastructure humanity has ever built.” And, Mills predicts, that cloud infrastructure buildup will serve as a platform on which the next generation of general-purpose technologies will be built.